Did Tom Sosnoff Invent 0 dte Options? Tom Sosnoff, Tony Battista, and Dylan Ratigan discuss 0DTE Options and how the CBOE got the idea for them /@CanadianOptionsTrader/

☑️ #30 Jun 27, 2025

The Hidden 0-DTE Secret Retail Traders Never See. How $0.01 Lotto Contracts Actually Print

@mikalche: They don’t teach you this on YouTube. You wont find anyone talking about this.

Everyone sees the 0DTE $SPY 620C at $0.01 and thinks it’s a YOLO.

Wrong.

It’s a weapon placed with intention. This is how pro 0dte players turn pennies into $250+ and why your fills never hit.

This is the $0.01 0DTE strategy institutions use and retail completely overlooks.

@_JaxCapital: Misleading, and damn near irresponsible content. Sad

@mikalche: Jack, what’s actually irresponsible is pretending 0DTEs are random YOLOs. The $0.01 contracts are placed into structure into flow, into traps, into volatility pockets. If you don’t understand that, maybe sit this one out. Some of us trade what’s actually happening, not what textbooks say should happen.

@_JaxCapital: There’s clearly an element of truth to the race that 0DTE can be BOTH random Yolos, and a systematic strategy in attempts to game the algorithms as the market becomes increasingly concentrated and computer driven. I’ll be the first to admit during the pandemic I even partook in such debauchery! However, I am NOT and never will be a trader so I’ll gladly leave that to folks like yourself who’ll I’ll admit are far better suited in that line of work than I and have a significant interest in increasing the degree of short term thinking in owning stocks. You’re correct in that I prefer long term ownership and compounding instead of seeking instant gratification and volatility of 0DTE. The potential downside risk and tax implications alone should be enough to dissuade any rational minded individual. Most importantly, to each their own, while I may not agree with the approach, I respect the hustle!

🙂

☑️ #29 Jun 20, 2025

S&P500 Forecast Indicator for SPX 0DTE

@StockMarketOptionsTrading: In this video, Eric walks through the updated SPX Daily Forecast Indicator from AlphaCrunching.com — a unique premarket tool designed specifically for zero DTE SPX traders. You’ll learn: How the forecast is constructed using 5-minute interval data from the past month. How to interpret the trend strength and directional bias for each trading day. How to compare current and previous weekly forecasts to detect trend shifts. A real-world example from Wednesday, June 11, showing how the bearish forecast aligned with actual market price action that day. This tool isn’t about predicting every move — it’s about helping you start each day with a data-backed directional bias to improve decision-making.

🙂

☑️ #28 Jun 12, 2025

Aries: ahead of their time ;-)

aries.com > discord > @yo_ai: Are we gonna be able to trade 0-dte spx options until close on this platform?

@Saad: Yes! You will full control over it and will provide you more options!

@Reda: I’ll be communicating an exact timeline soon.

+ Related content:

aries.com (Date?): [Excerpt] Announcing the Launch of Aries.com: Secure Your Place in Line.

Today, we’re thrilled to announce that Aries.com is live! After months of dedication, ingenuity, and hard work from our exceptional development team—and the invaluable input from our loyal community of users—Aries is preparing to introduce an entirely new suite of products designed to revolutionize trading and investing for traders, investors, and developers alike.

In just a few months, we’ll be releasing Aries Infinite, Aries Engine, and Aries Mobile to the public. Each product offers powerful, intuitive technology to elevate the trading experience and empower users to trade, create, and build without limits. As we approach launch, we invite you to sign up for the waitlist to secure your place in line and be among the first to experience the future of trading.

Here’s a look at each of the products we’re excited to bring to you soon.

Source: Aries Financial, Inc.

aries.com: [Excerpt] "about us" shouldn't be an afterthought.

To understand what we’re building and who we’re building it for, we’d like to tell you about where we came from. Aries is a close-knit team of developers and traders who’ve spent our lives building fintech. We come from different countries and backgrounds, but we’re united by a shared belief: making it easier to innovate in fintech will lead to more great ideas. Right now, fintech faces an innovation problem. Developers are bogged down by challenges unique to the industry—regulatory hurdles, data licensing fees from multiple vendors, infrastructure complexity, KYC/AML compliance, licensed customer support... the list goes on. By the time developers piece together all the necessary components just to build a platform, they’re often out of time and money. This problem isn’t unlike what independent game developers faced several years ago. Before they could focus on creating characters, environments, or gameplay, they first had to build a physics engine—a daunting task that killed many projects. Then Epic introduced Unreal Engine, a ready-made platform that allowed developers to jump straight into creating their games. It sparked a renaissance in independent game development. In the same way that Epic built Fortnite to showcase the power of Unreal Engine, we built Infinite to demonstrate what’s possible with the Aries Engine. At Aries, we’re developers and traders, and we believe in empowering people—giving them more control over their money and more advanced technology to do it with. We believe in developers and their ideas. We know that when developers have the right platform, they create amazing things. And as excited as we are about what we’ve built, we can’t wait to see what you do with it.AD

ASTRA PER ASPERA.

Made with ❤️ by Reda, Pash, Keith, Saad, Bill, David, Hussein, Alex, Phil, Nsikak, Matus, Jeet, and team.

🙂

☑️ #27 Jun 10, 2025

Want a 0 DTE portfolio that actually survives volatility?

@zerodaymark: Forget “one-size-fits-all” — markets chop, trend, and sometimes go full chaos mode. You need a portfolio that adapts, not just survives.

After trading this space for years, here’s how I build a resilient, revenue-generating 0 DTE portfolio — designed for all market regimes:

The Workhorse – High-Frequency Condors (50%) Your steady-income engine. These low-variance trades run multiple times daily, ideal for sideways or grinding markets. Think consistent premium capture — day in, day out.

The Opportunist – Trend Followers (25%) When the market moves, these hit big. A mix of credit spreads and long deltas, tailored to capture momentum. Lower frequency, higher payoff.

The Airbag – Long Straddles/Strangles (25%) Your built-in convexity hedge. You hope they don’t fire often — but when vol spikes or news hits, these shine. Protection that pays when it matters most.

The key? It’s not about predicting — it’s about preparing.

Pre market report to distill options positioning including 0dte

Zero Sum Nasdaq: Starting today we’ll publish the pre market report for SPX / NDX / ES / NQ / VIX / QQQ / SPY

Our record of pivots and targets have been very good- published on X (at nqmarketprofile) - For example, yesterday our premarket report was a clear ‘buy the dip at open’ to 21880 NQ — this is where the market topped.

To keep things consolidated we’ll publish a detailed pre market report to distill options positioning including 0dte to provide an easy to follow FREE roadmap for trading ES/NQ Futures.

Report will be published around 13:15 GMT or about 8:15 EST

Data pulled from MenthorQ - I have no affiliation with this service. The interpretation is my work and not intended as trading advice or recommendation to purchase or otherwise trade any securities, purely for educational purposes.

I aim to provide the most accurate NQ report on Substack

Nam Nguyen Ph.D.: New research and CBOE data show that 0DTE (zero days to expiry) options don’t increase market volatility, thanks to balanced trading flows and minimal net gamma exposure.

Both institutional and retail traders use similar strategies, but differ in timing and risk management.

While institutions open trades earlier and hold longer, retail traders are more active throughout the day, often managing risk more hands-on.

Subscribe for more data-backed information like this.

@StockMarketOptionsTrading : In this video, I walk through a live SPX 0DTE trade using my “Forest Trading” method — a strategy designed to build risk-free trades by layering credit spreads to create wide profit zones (aka green grass 🌱). The goal? Minimize downside while locking in gains as price moves. I also highlight two key indicators I use to guide these setups: Alpha Crunching Daily Forecast – Built on 5-minute data to reveal intraday tendencies. A new version is coming soon! The Daily Forecast is what I used as a premarket indicator shown in the video. 🎯 Try it now at

The fundamentals of trading zero-days-to-expiration (0DTE) options

@TradeStation: Zero-days-to-expiration (#0DTE) #options offer fast-moving potential for strategic traders. Learn how to think in minutes instead of months, with our new guide to this fast-moving strategy. Find out how they work:

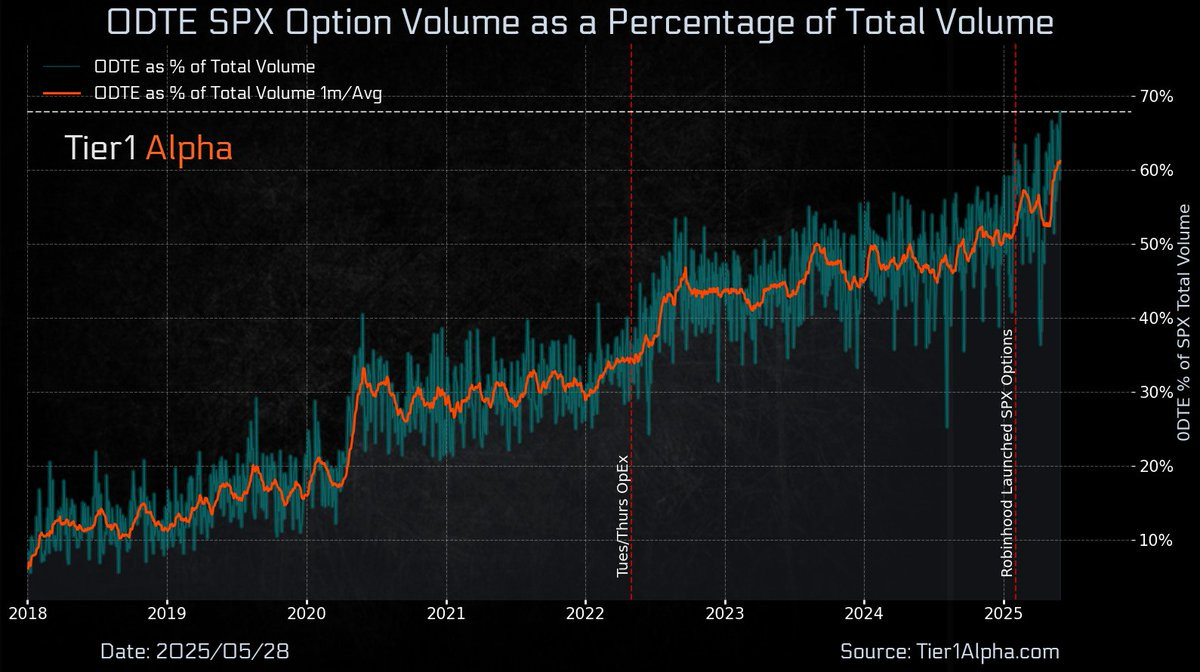

@t1alpha: Yesterday was another all-time record for 0dte contracts, pushing 68% of relative options volume for $SPX. A weapon of choice in an increasingly myopic market.

0-DTE call flow is a powerful, reflexive source of market lift—almost an “infinite-money glitch” for SPX during U.S. hours. But it isn’t bulletproof. Sharp vol repricings, big macro surprises, or dealer gamma flips can all shut off the bid-stream. For traders looking to fade the moves, the hurdle to be bear-leaning intraday is extraordinarily high—until one of those kill-switches fires.

fiatelpis.com: [Excerpt] Fiat Elpis Macro Fund. Easy access to best‑in‑class macro hedge fund trading with a proven track record above 1400% since May 20201

🙂

☑️ #19 May 24, 2025

Impact of Zero DTE Options on the Market

via Harbourfront Quantitative Finance: [Excerpt]We do not find evidence that the 0DTEs option open interest gamma propagates or unconditionally increases the underlying index volatility. Instead, our results suggest the opposite: higher 0DTE and other short-term options open interest gamma, measured by combining open interest at the market open and options’ dollar gammas shortly after that, is associated with lower realized volatility within the day and does not propagate overnight and lagged intraday volatilities…

papers.ssrn.com (2/5/24): [Abstract] We study the recent explosion in trading of same-day expiry (0DTE) options on the S&P500 index and examine if this trading activity is destabilizing for the underlying index. We find that Market Makers’ inventory, as measured by the net gamma of their positions, is on average positive and negatively related to future intraday volatility. We also show evidence suggesting that positive (negative) Market Makers’ inventory gamma strengthens intraday price reversal (momentum). Our empirical evidence is consistent with delta-hedging but inconsistent with information-based trading.

🙂

☑️ #18 May 20, 2025

Interest Rates (0DTE): every day of the week

@Interest_Rates: Coming June 16: Tuesday and Thursday Weekly Treasury options. Building on the success of existing Mon/Wed/Fri Weeklies (633K ADV YTD), Tue/Thu Weeklies aim to meet growing demand for short-term options by providing market participants with option expiry every day of the week.

+ Related content:

cmegroup.com (update; 5/23/25) (pdf): New Product Summary: Initial Listing of Tuesday and Thursday Treasury Weekly Options - Effective June 16, 2025.

@GammaEdges: The secret to predicting SPX market direction isn't on your price chart. It's hidden in the flow of SPX 0DTE options volume *throughout* the trading session. Here's how to unlock this edge & spot trending vs choppy days BEFORE price confirms. It's dead simple. Stick with me:

Daily Dynamics: Zero DTE volatility throughout the day

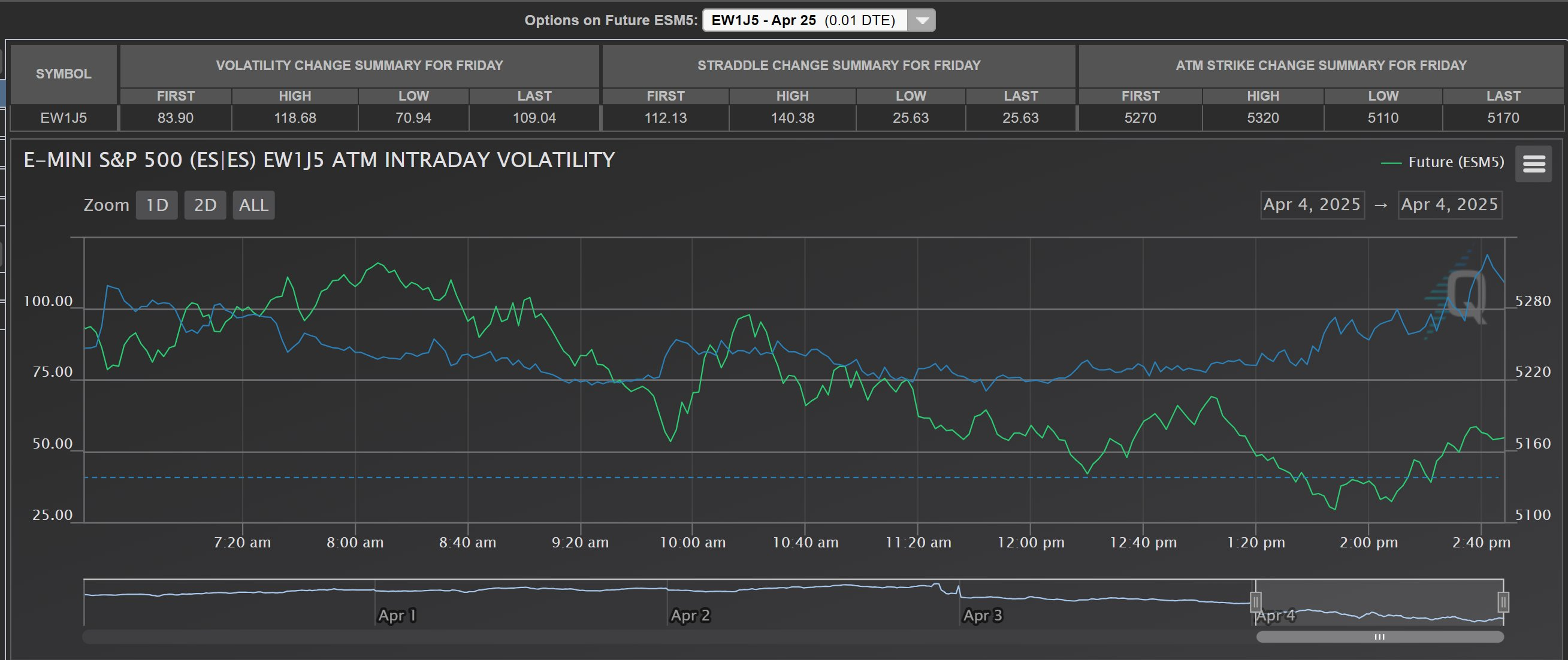

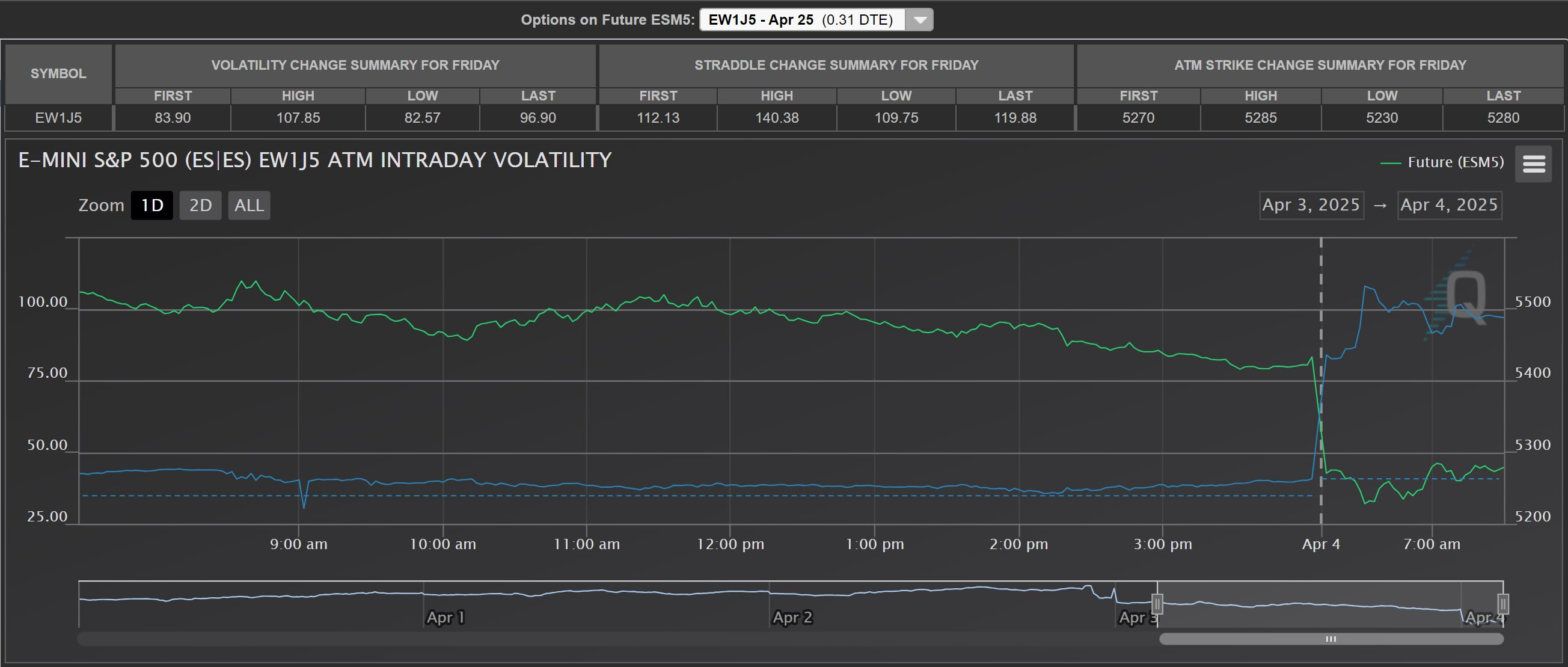

tastylive.com > Slides: [Excerpts] MAY 15, 2025. In today's discussion, Tom Sosnoff and Tony Battista dive into zero-day-to-expiration (0 DTE) trades, highlighting how implied volatility behaves throughout the trading day, often declining as expiration approaches. The duo discusses key findings from a two-year study on intraday volatility, emphasizing that regardless of the opening volatility, premiums tend to decrease rapidly as the day progresses, impacting option strategies effectively.

When IV started low, it typically took slightly longer to start coming out. Looking at the -20% line, the average relative IV crosses it around 10:30 in low IV but closer to 10:00 overall. Still, by the end of the day, relative IV collapsed all the same.

Higher opening IV was more erratic, with wider standard deviation. Typically premiums would decrease rapidly, but this was less reliable.

However you choose to play your O DTEs, these charts can give you a handle on anticipating how long you want to stay in and let the premiums decay.

spotgamma.com: [Excerpt] How Does 0DTE Trading Impact the Equity Market?

The price action seen on 5/12 is not unique – it is something that we monitor on a daily basis. To this point, we generally believe that 0DTE trading brings mean reversion to SPX price action – meaning the 0DTE flows essentially act to “buy the dip, and sell the rip”. We will be detailing this view in future posts.

We have seen a pattern of a reduction in 0DTE flows when volatility spikes, as witnessed during the early-April market turmoil. We believe this is both because 0DTE traders step back during times of extreme volatility, and there is an increase in longer dated options activity as longer dated hedge demand increases.

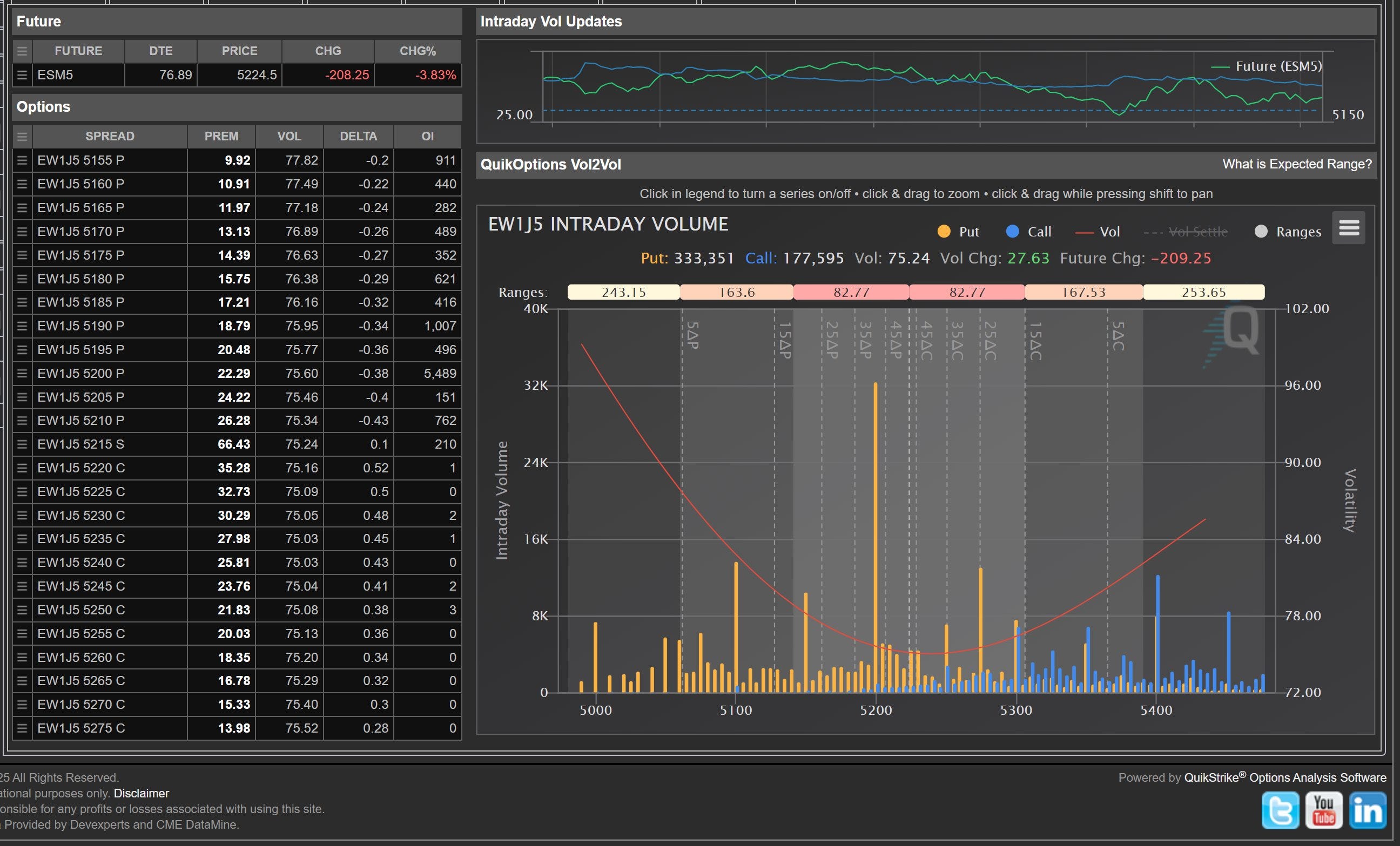

Gamma Capture S&P 500 intraday volatility over the next 30 minutes. For OTE ontions traders

options tree: Gamma Capture 0DTE Strategy Finder. By Lou Pellathy and Dr. Rob Navin.

Gamma Capture Vol:

The innovative measure uses tick data to decide whether same day SPY 0DTE option’s implied volatility is high or low. Options containing lower (higher) levels of implied volatility will result in cheaper (more expensive) option prices.

SPX zero day to expiry (0DTE) options trading have grown more than five-fold over the past 3 years, now averaging almost 2M contracts a day. What is driving that growth? Increased utility and wider adoption are two big drivers, with retail powering much of the increase. We estimate that retail now makes up around 50-60% of SPX 0DTE trading.

In this report, we take a deep dive into retail and institutional trading characteristics – what they’re trading, how they’re trading, and the risk profiles of each group. One notable takeaway is just how sophisticated and disciplined retail investors have become in 0DTE trading and the multiple ways they have in managing their risk.

We also take a look at how investors have been navigating the recent market volatility, with SPX intraday volatility surging to 2008 GFC highs. Not surprisingly, retail has pulled back as a percent of overall volume – similar to what we saw in past episodes of sudden volatility spikes – with the retail share of 0DTE trading dropping from 57% to 47% in early April. However, just like in previous episodes, retail investors have returned once volatility has abated, with the retail share jumping back up to 60% in recent weeks. We attribute much of the resilience in 0DTE trading to the fact that over 95% of all 0DTE trades are done in a limited risk format (either long options outright or short via spreads) where the max loss is known at the point of entry. Only 4% of SPX 0DTE trading is in naked short options.

Lastly, we take a look at 0DTE market maker hedging flows and whether they could be contributing to the recent volatility. Instead, we find that customer activity continues to be extremely balanced in 0DTE options, and as a result, net market maker gamma hedging remains de minimis, representing at best, just 0.2% of the SPX daily liquidity. For more, see full report here.

@VolSignals.com (update;5/4/25): A few things going on there @everyone -

basically, any time the market moves significantly, Cboe trots out Mandy Xu for a PR blitz to defend the honor of 0DTEs. This is typical and while I don't have any issue with 0DTE trading, I don't think they are problematic for market structure, I do think they dodge the point and use spurious logic/data to back their claims. They could do better here.

I also noticed that last segment about April 4th and April 9th volumes... I thought the validation she leaned on was absurd.

Essentially...

the claim is that at most the MM gamma was 2.1bn on a day when futures traded 940b notional, market maker hedging activity must only account for 0.2% of "liquidity"

This is either an intentional misdirection or a very poor understanding of market making as a business, since a one and done notional gamma number has virtually nothing to do with the actual amount of liquidity provided or taken cumulatively throughout the trading day.

For Mandy's claim regarding proportional liquidity to be sound, it would literally mean that:

1. SPX MMs all collectively hedge one book together... never trading MM vs MM (dealer v dealer) in the futures themselves (of course, this is not true).

2. SPX MMs have one notional gamma exposure collectively, and this is hedged once per day, regardless of the actual underlying movement of the index. (Remember notional gamma is a measure of notional delta exposure the MM would expect to get long/short on a 1% move in either direction—that is also not how the industry hedges. Especially not in 0DTE).

3. There is no scalping implied... no trading "back and forth"

but hey... at least we all agree that dealers hedge 0DTE with futures!

cnbc.com (4/14/25): Zero-day options are fueling the unprecedented volatility on Wall Street amid tariff chaos.

go.cboe.com (pdf; 9/7/23): Much Ado About 0DTEs: Separating Fact From Fiction. Evaluating the Market Impact of SPX 0DTE Options.

🙂

☑️ #11 May 1, 2025

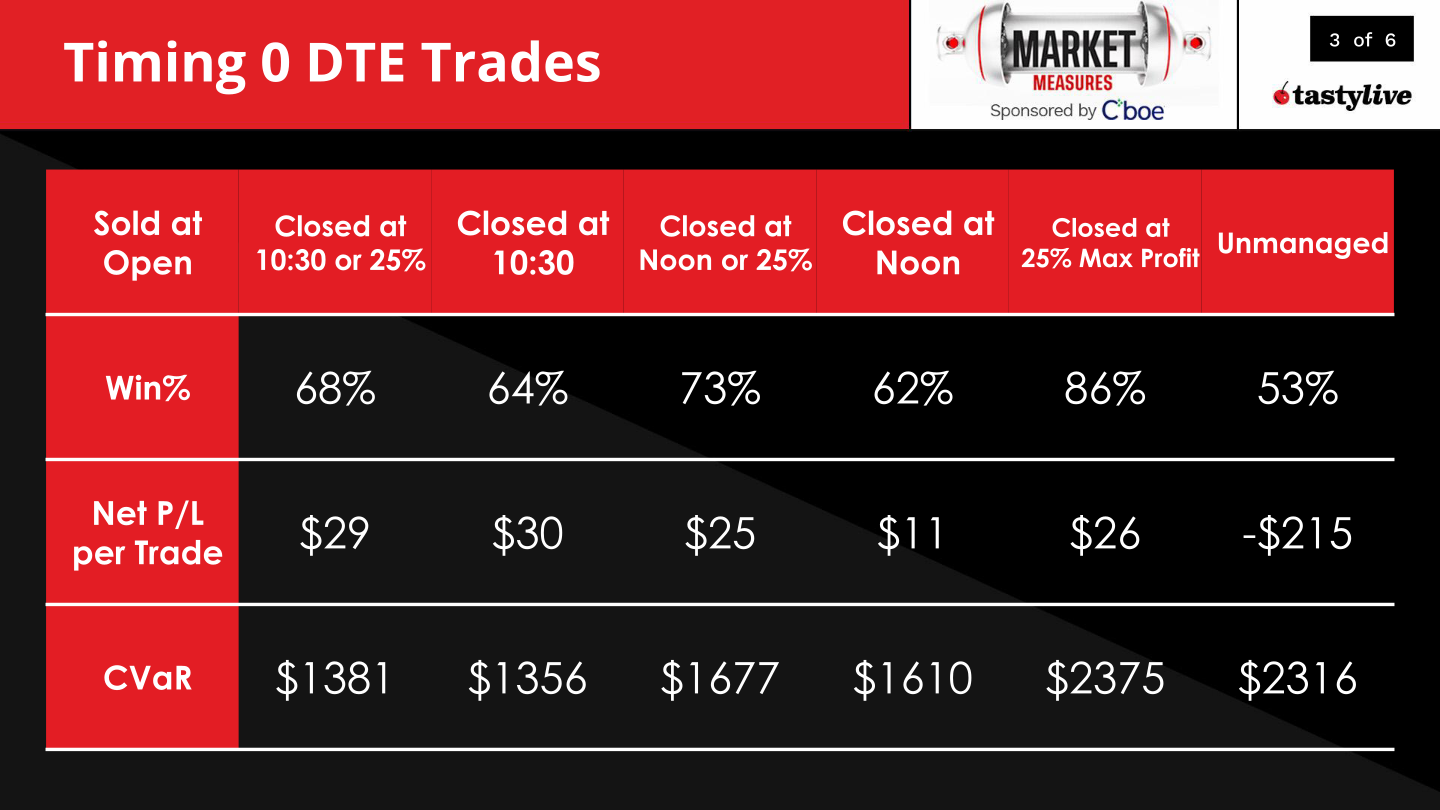

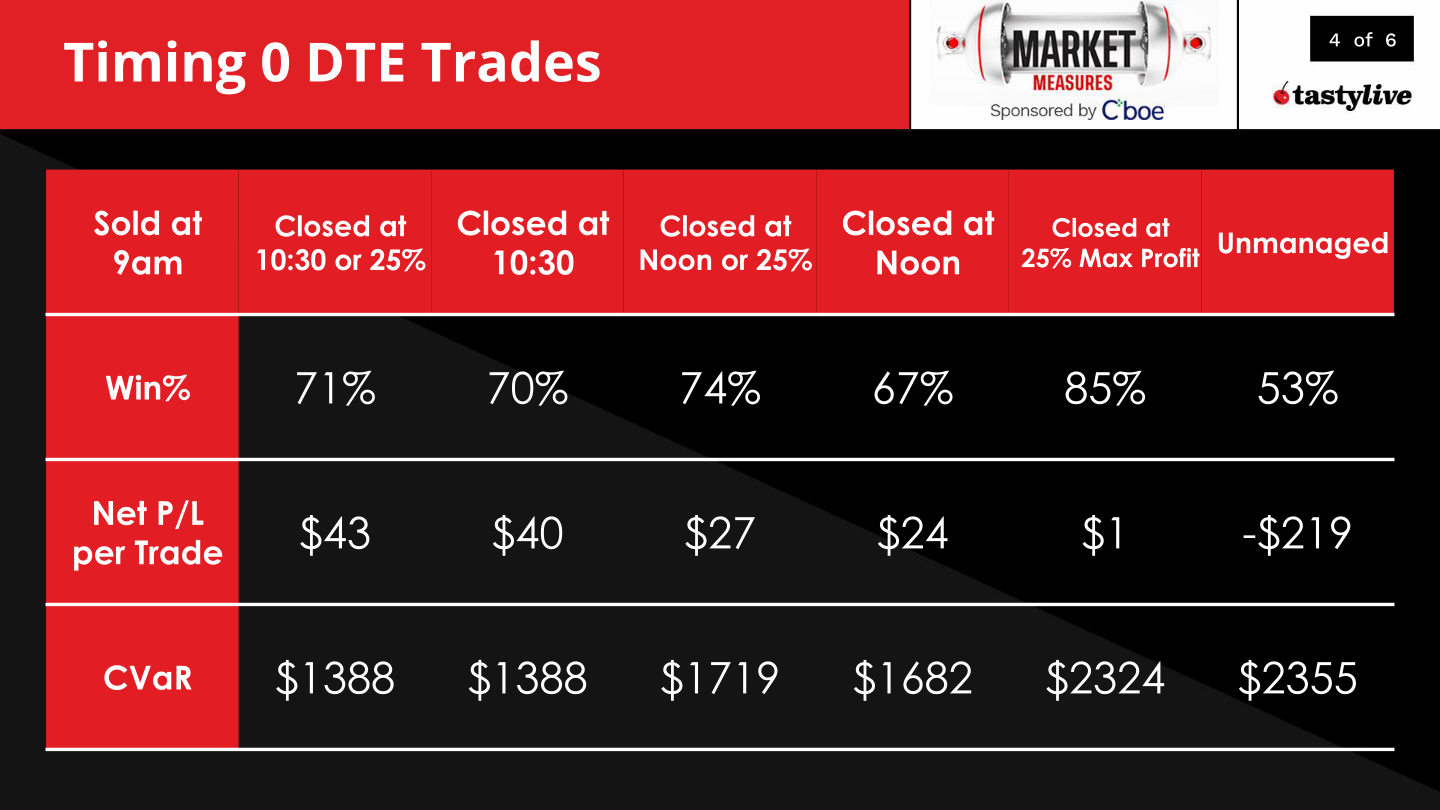

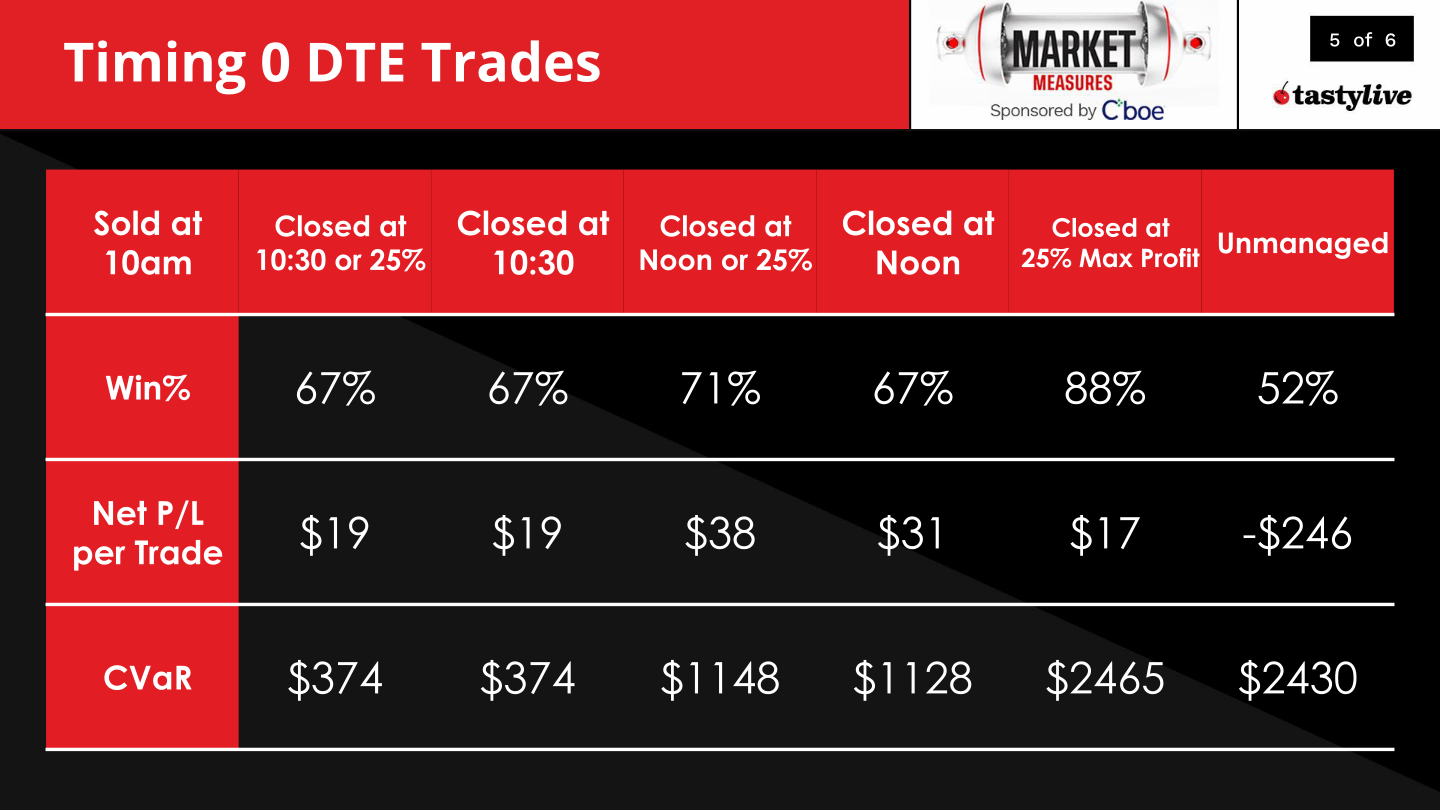

Timing 0 DTE Trades

tastylive.com: [Excerpts] New research on zero days-to-expiration (Zero-DTE) options shows selling iron condors at specific times can significantly impact profitability.

The study:

Using 2 years of data in 0 DTE SPX options collected every 10 minutes.

Each day, examined selling iron condors at market open (8:30am), 9am and 10am every day with either 304 short strikes and wings at $30 past there.

Considered closing trades at 10:30am, noon, or without a fixed exit time. Both paired with 25% profit targets or just based on exit times.

All trades were assumed to exercise at mid-price.

Time-based management is a promising addition to our 0 DTE mechanical arsenal. Closing positions at 10:30 AM, win or lose, resulted in some of the most profitable outcomes we have seen.

The 'half-hour' trades, opened at 10:00 AM and closed at 10:30 AM, didn't generate as much profit as staying until noon, but they avoided the biggest losses while still being profitable, which is appealing in its own right.

Pairing this time management with profit target limit orders, even when rarely triggered during a short time window, was generally beneficial for profitability and consistency of winning trades.

Once again, it seems the key to success with O DTE short premium trades is rapid trade management, however you achieve it. What 0 DTE trade mechanics have you found most successful?

optionalpha.com (8/20/24): [Excerpt] With the popularity of 0DTE, traders are flocking to options assuming prices decay at the same rate all day. But is this actually what happens? Let's see.

Highlights

Time decay is non-linear, accelerating rapidly in the afternoon.

Significant theta decay in 0DTE options occurs primarily after 3:30 PM ET.

OTM options decay faster than ATM and ITM options.

Volatile markets prolong option premium retention, especially during extreme events.

Entering trades later maximizes decay, reducing unnecessary directional risk.

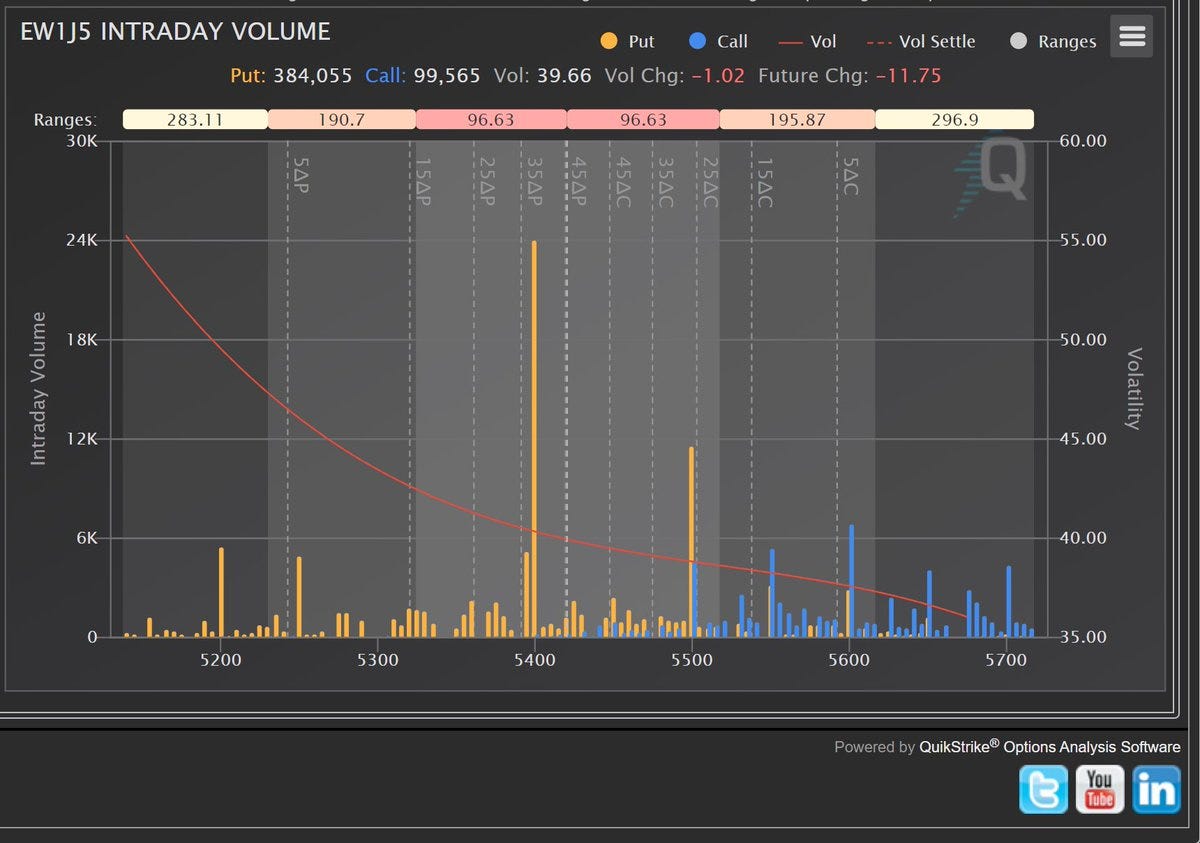

cmegroup.com: CME Equity Index Options on Futures Bloomberg Cheat Sheet. Friday Weeklies:

Friday Weekly 1 (EW1) > EWJ5

Friday Weekly 2( EW2)

Friday Weekly 3 (EW3)

Friday Weekly 4 (EW4)

Week code: week of the month 1 (3/31-04/04)

Month code: J (April)

Year code: 5 (2025)

🙂

☑️ #7 Apr 1, 2025

Since these options have a 6.5-hour lifespan, you must trade them as bet options

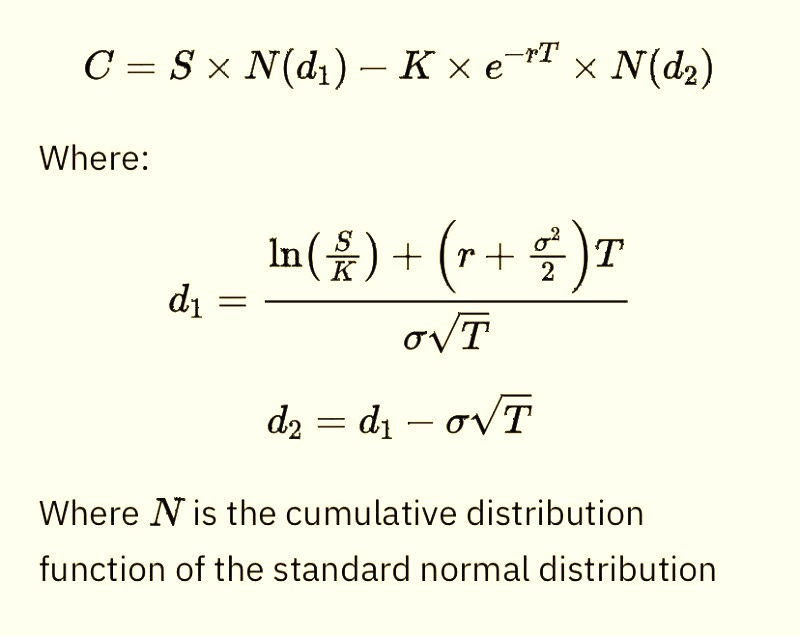

steepgreeks.net: [Excerpt] 0 DTE SPX Options: Not What You Think.

These options have become very popular, especially in the retail trading space. Therein lies the paradox. These options are essentially exotic options that trade-off pure probability, not Vol & Greeks. If I had to pigeon-hole them, I’d call them a Cash-or-Nothing European Digital. As such, the only real way to value them is to calculate their N(d2). In the context of option pricing, "N(d2)" represents the risk-neutral probability that an option will expire in-the-money (ITM), meaning the underlying price at expiration will be above the strike price.

Since these options have a 6.5-hour lifespan, you must trade them as bet options. Now, in my case, I do run a contextual screen to determine the current trading environment (vol-compression vs. vol-amplification) in order to utilize the appropriate forward distribution of daily returns. My distribution is not “risk-neutral; therein lies my edge in trading these things.

It’s not surprising that the brokerage firms & the exchanges are marketing these things to the retail crowd. It’s a cash cow. If you’re going to trade them, forget about Vol & Greeks.

It’s a bet market!

+ Related content:

steepgreeks.net: The Delta House (ΔVθ). A mentorship community to connect and learn.

Zero DTE refers to trading (or analyzing) options on their last day of expiration (opex).

DTE means days to expiration, and so “zero DTE options” are simply options on their last day before either expiring worthless or with some value.

Zero DTE options have extremely high gamma levels (how quickly the directional exposure of an option changes based upon success with direction) and extremely high theta levels (the accelerating pace of the time decay of an option’s price).

As long as most institutional players are short zero DTE options, then this has a stabilizing effect for the market during the day; overnight gaps lack this liquidity protection, with liquidity meaning enough bids and offers available to keep prices stable.

Advanced: Zero DTE and Market Gamma

As of 2022, zero DTE trading has taken center stage in the discussion. Institutions and retail volume alike have flowed out of longer-dated contracts and into ultra-short duration contracts with single-digit days to expiration. Given that gamma (acceleration of directional exposure) becomes stronger approaching expiration, the rise of zero DTE means that more volume (the total shares being traded) is now using more gamma.

If this zero DTE volume becomes too extreme, then it can be especially destabilizing for the market if aggressors (those buying at or above the ask or selling at or below the bid) are mostly long zero DTE options. This is because that makes dealers short those same zero DTE options, and this is the period where being short gamma (from being short options) is as dangerous as it gets, prompting violently large market orders (from market makers) in the direction of the underlying security’s trend.

In other terms, this means that if aggressors are mostly short DTE options (and dealers are long), then this adds strongly positive market gamma. For the most part, this can effectively keep prices contained in a relatively small range.

Expert: Zero DTE and Volatility

Below is proof of how much zero DTE has affected the nature of the volatility surface (time and strike/delta each on their own independent horizontal axis vs IV% on log scale vertically), with comparisons below of 2023 in blue to 2022 in orange. Log scale is used so that there can be infinite room for the expansion of volatility–to make room for how volatility can technically expand infinitely.

Caption: 3D volatility surface retrieved from Trader Workstation

The above visualization of the 3D surface is what it looks like with all the volatility smiles connected from each day, showing that skew.

The volatility surface of SPY is almost identical to how it was at this time last year (mid March of 2022). Even the strike placements are lined up the same. The big difference however is what is happening in the zero DTE segment, in which case we can see spiked IV (implied volatility) at-the-money and also out-of-the-money on the put side.

This is the new arena we are in. As a refresher on the mechanics, this extreme IV is partially offset by how a smaller and smaller slice of vega is part of the equation for how options are priced as they approach expiration. This means that IV is higher (which raises the price of options).

However, this extreme IV on the last days of expiration, as shown on the surface, is merely amplifying an ever-smaller area of the pie chart on what makes up the price of the option. This is the tradeoff.

On the other end of the term structure (IV compared to time), longer-dated options have larger and larger slices of vega, which means that their prices are more sensitive to changes in IV.

It follows that, with zero DTE options, they have the smallest amount of vega, which is the part of the price that gets amplified by IV. Eventually, this slice is worth zero at the contract’s actual expiration because there is only intrinsic value left (how much the spot underlying price outperformed the strike price minus the debit paid to buy the option). This dynamic of the vanishing slice of the option’s value (amplified by IV) must be considered when trying to trade volatility on zero DTE options.

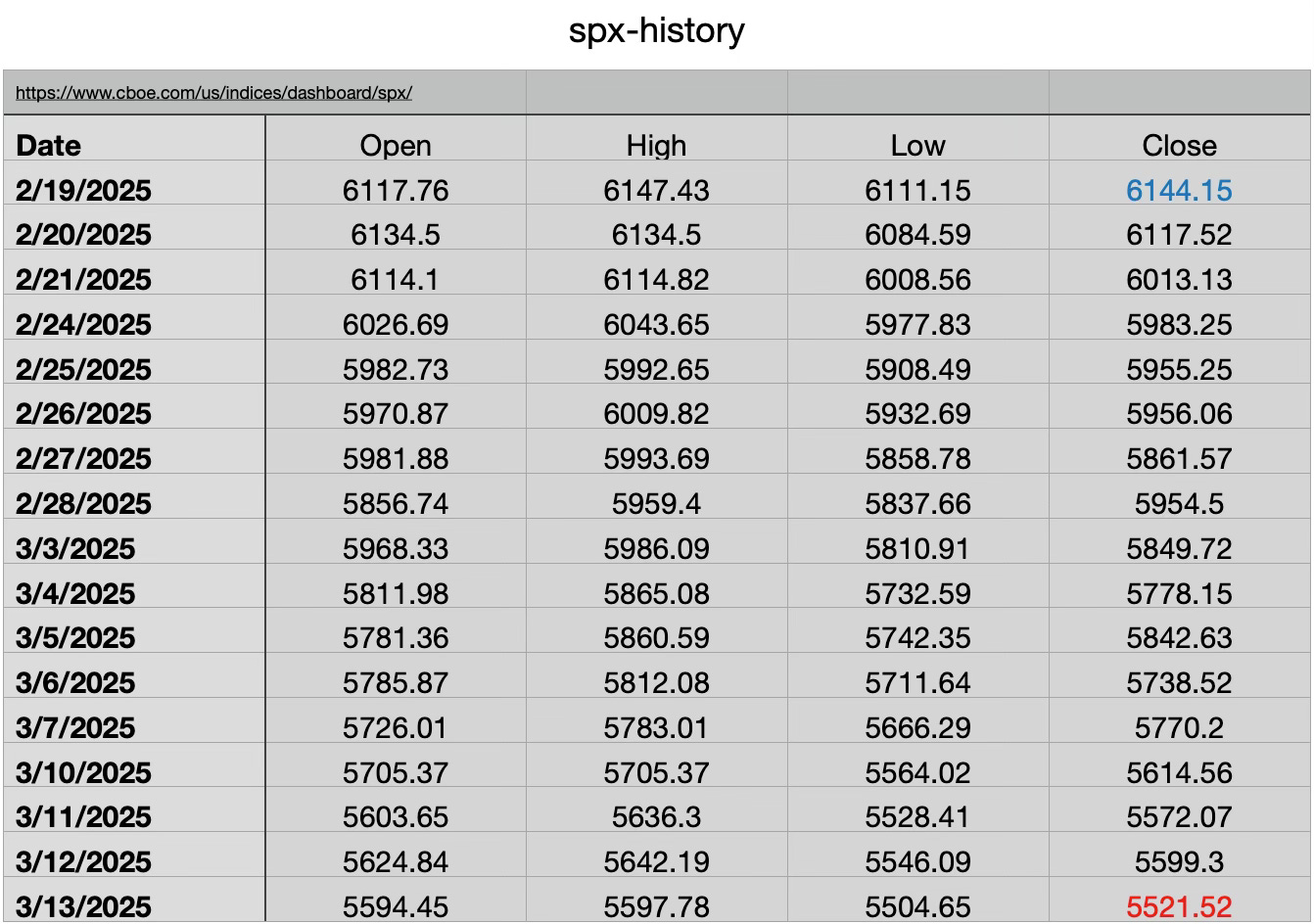

This is the first 10% drop within 30 days that has occurred with the existence of 0DTE options

@market_sleuth: Fun Fact. History was made with the recent 10.5% $SPX drop. Since the inception of the VIX there’s never been a 10% drop in 30 days with the VIX staying under 30. Ever. Until now.

⚡️

@CAndreisen: This is the first 10% drop within 30 days that has occurred with the existence of 0DTE options. It will be much harder for IV on 30-day and longer dated expiry options to rise when large institutions can avoid paying for unnecessary theta and just buy shorter dated protection.

+ Related content:

cboe.com (2/19/25-3/13/25)): Standard & Poor's 500. SPX_history.csv

🙂

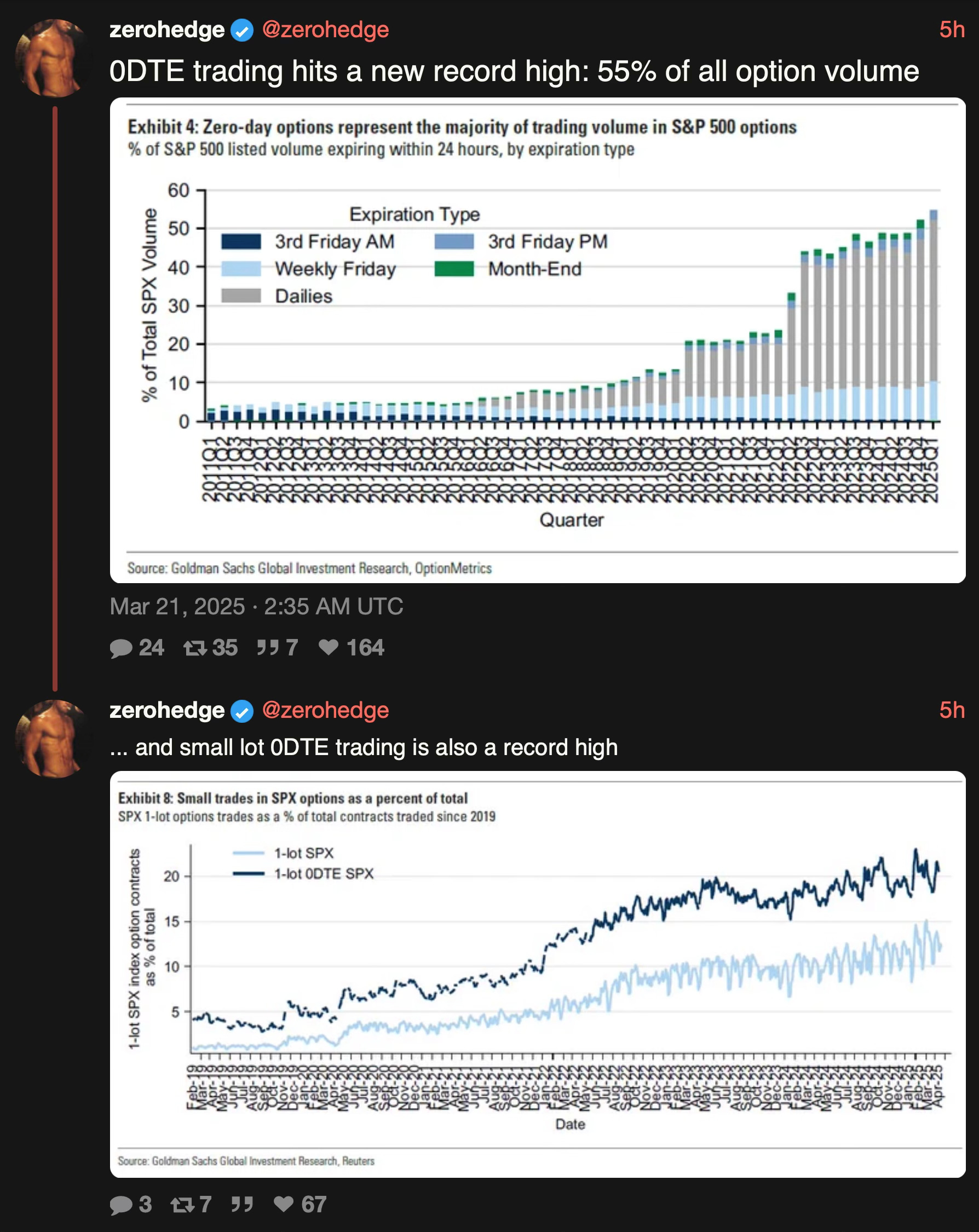

☑️ #4 Mar 21, 2025

55% of all option volume

xcancel.com/@zerohedge: 0DTE trading hits a new record high: 55% of all option volume... and small lot 0DTE trading is also a record high.

🙂

☑️ #3 Mar 19, 2025

March has been the worst month in years for ODTE option buyers

@VolSignals: A lesson in how "not" to trade 0DTE options. "Chart shows monthly total P&L (% of spot price) of buying a 0DTE SPX Straddle at 9:45 AM each day and holding it until the close"

🙂

☑️ #2 Mar 11, 2025

Observations & Insight

johnlothiannews.com: [Excerpt] I asked if there was an update about single name 0DTE options since last year’s OIC conference and was told there have been discussions, but there are still problems to be solved. One of the biggest problems is how to deal with early exercise, or exercise at all. One suggestion was to offer cash settled 0TDE single names, but the brokerage firms have said it would confuse customers to have two choices. My suggestion is to make the strike prices for the cash settled version every five dollars and the physical settled on the $10.00.

iongroup.com: [Excerpt] Why investors are betting big on same-day expiries.

Options trading has boomed, with equity options at the forefront.

Zero day to expiration (0DTE) contracts have gained the most traction to hedge risk.

Investors and traders need to have a well-defined strategy and understanding of these complex contracts.

While 0DTEs share benefits with the equity options family, they also have the advantage of having the expiration date set on the same trading day. So, there are opportunities for quick decision-making and potentially strong returns. This is especially advantageous for premium sellers, who can capitalize on the extremely fast theta decay (that is, the rate of decline in the value of an option over time).

Other selling points include a lower premium compared to options with longer expiration dates due to their shorter expiration timeline and greater flexibility. This is because traders can take profit son short-term market movements without the long-term commitment that other options require. Moreover, 0DTEs offer a targeted solution to mitigate intraday risks.

This Study Changed How We Trade 0 DTE At The Close

@tastyliveshow: New research analyzing 4,000 trading days reveals surprising patterns in the S&P 500's final 15 minutes. Data shows 95% of moves stay within 0.5%, with Tuesdays showing the smallest range. March had the most outliers, while December and January were calmer. Compelling viewing for zero-DTE traders managing end-of-day positions.

fiatelpis.com: [Disclaimer] Past performance is not indicative of future performance. All information on this website is for educational purposes only and is not intended as investment advice.

The analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security.

To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice.

To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation to buy, sell or hold such investments.

This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Any trading symbols displayed are for illustrative purposes only and are not intended to portray recommendations.

, when time passes without our strikes being threatened, or from v ('vega'), when implied volatility goes down. • For 0 DTE trades, this means looking for an IV contraction over the course of the day. • How has 0 DTE implied volatility typically behaved throughout the trading day?")

or low (below). • All times are Chicago.")

while retail is more active in iron condors and butterflies. How they trade, however, can be quite different. When we examine the intraday trading patterns of retail vs. institutional, we can see that institutional investors are much more aggressive in opening positions at the beginning of the day with 18% of all opening trades happening in the first 30 minutes. Institutional opening activity trails off significantly after that. In contrast, retail investors are active both at the start as well as the end of the day, with ~12% of all opening trades occurring in the first 30 and last 30 minutes of the day. The U-shaped volume curve for retail ODTE activity very much resembles the typical intraday volume curve for equities.")

{kind=link}

{kind=link}

{kind=link}