Until the early 1980s, there was only one conduit for publicly traded companies to return cash to owner, and that was paying dividends. In the early 1980s, US firms, in particular, started using a second option for returning cash, by buying back stock, and as we will see in this section, it has become (and will stay) the predominant vehicle for cash return not only for US companies, but increasingly for firms around the world.

–Aswath Damodaran

Securitiex on Substack is a Darwinex Zero Affiliate Partner

ASSETS YOU CAN TRADE: Currencies, Indices, Commodities, Treasuries, Bitcoin (CME and Eurex) US Stocks/ETFs (Cboe) and CFDs

Join Darwinex Zero and transform your strategy into an investable index with certified track record (use the code DZ20OFF for 20% off): DZ20OFF

☑️ #16 Oct 31, 2024

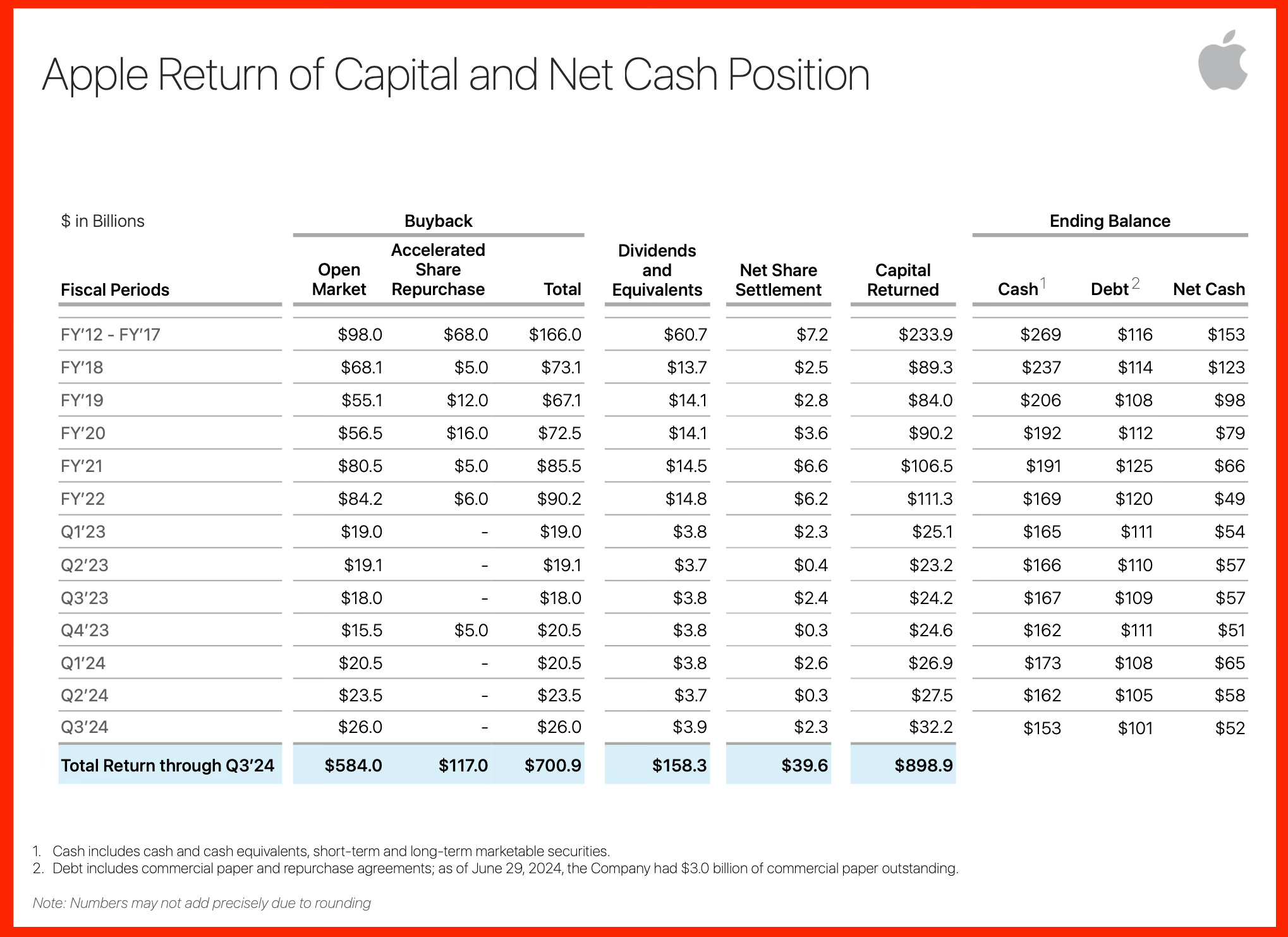

Capital Return History: AAPL

investor.apple.com: [Copied & Pasted] Investor Updates > Additional Reports > Apple Return of Capital and Net Cash position

[Excerpt] “Our record business performance during the September quarter drove nearly $27 billion in operating cash flow, allowing us to return over $29 billion to our shareholders,” said Luca Maestri, Apple’s CFO. “We are very pleased that our active installed base of devices reached a new all-time high across all products and all geographic segments, thanks to our high levels of customer satisfaction and loyalty.” Source: Apple, Inc.

🙂

☑️ #15 Oct 7, 2024

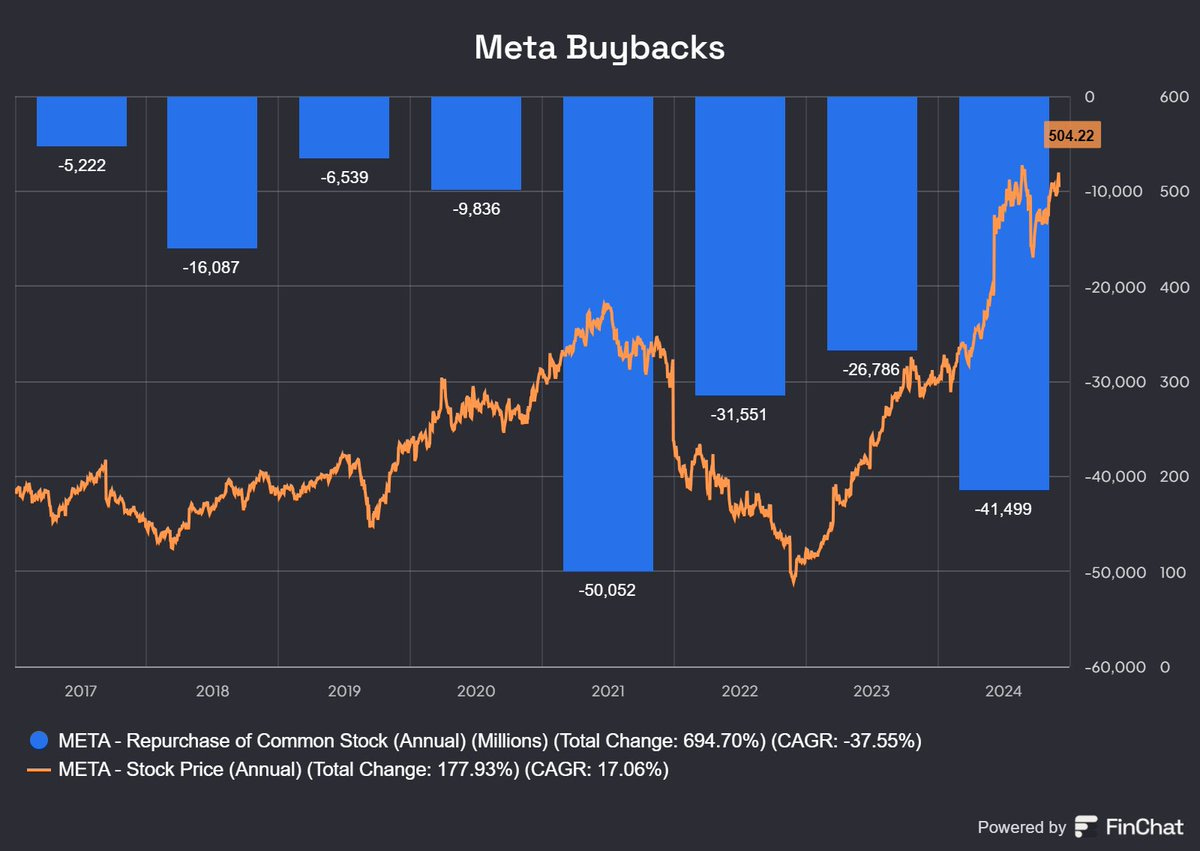

META - Repurchase of Common Stock (Annual) (Millions) (Total Change: 694.70%)

@RihardJarc: $META $600 today. I remember when people were very critical of the $50B buybacks back in 2021 in the $300 range.

Looking back Zuck was right again and long-term shareholders were rewarded.

It has been my biggest position then and continues to be. Excitied for $META's future.

Buybacks are a big driver of stock market returns.

🙂

☑️ #13 Aug 1, 2024

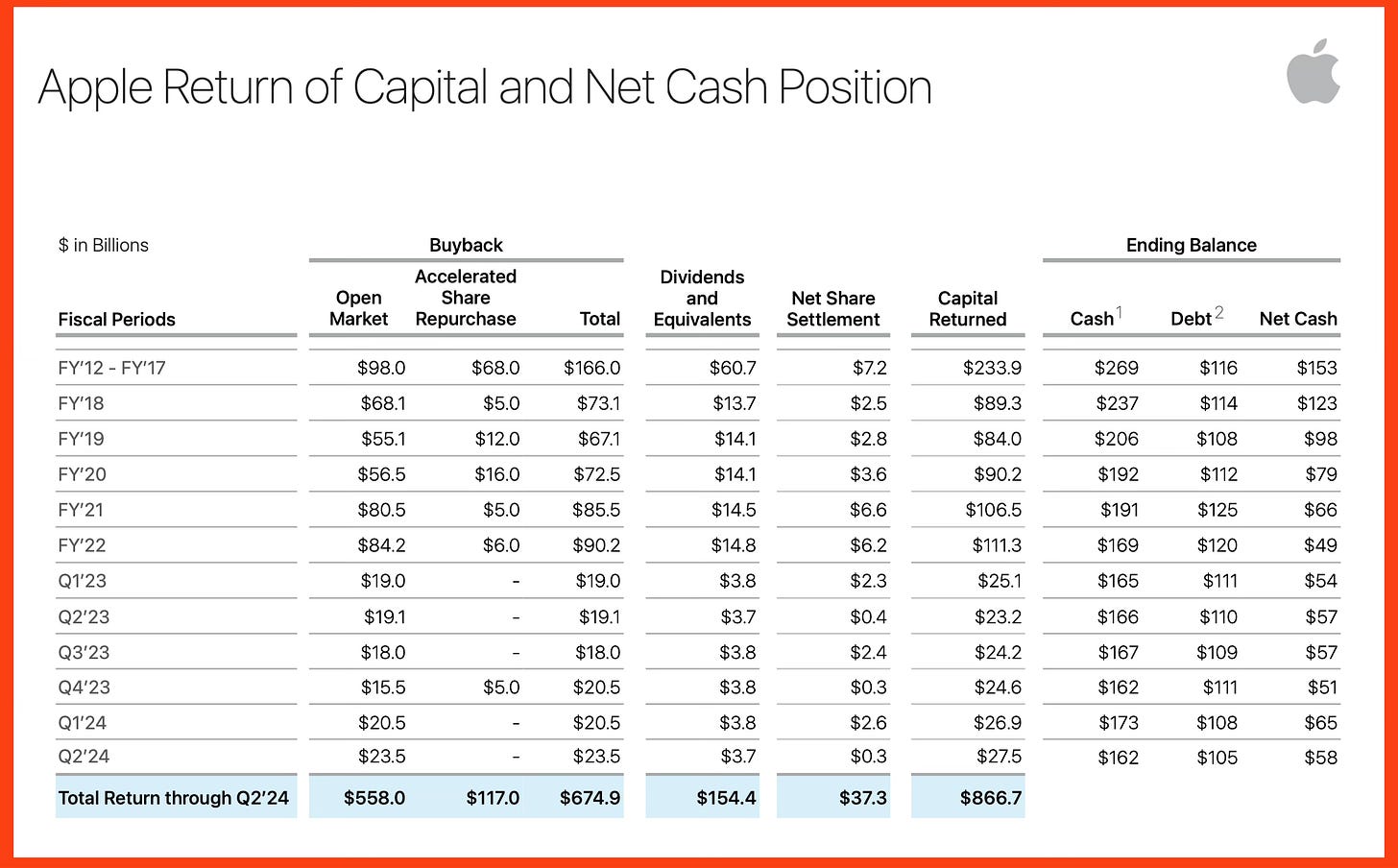

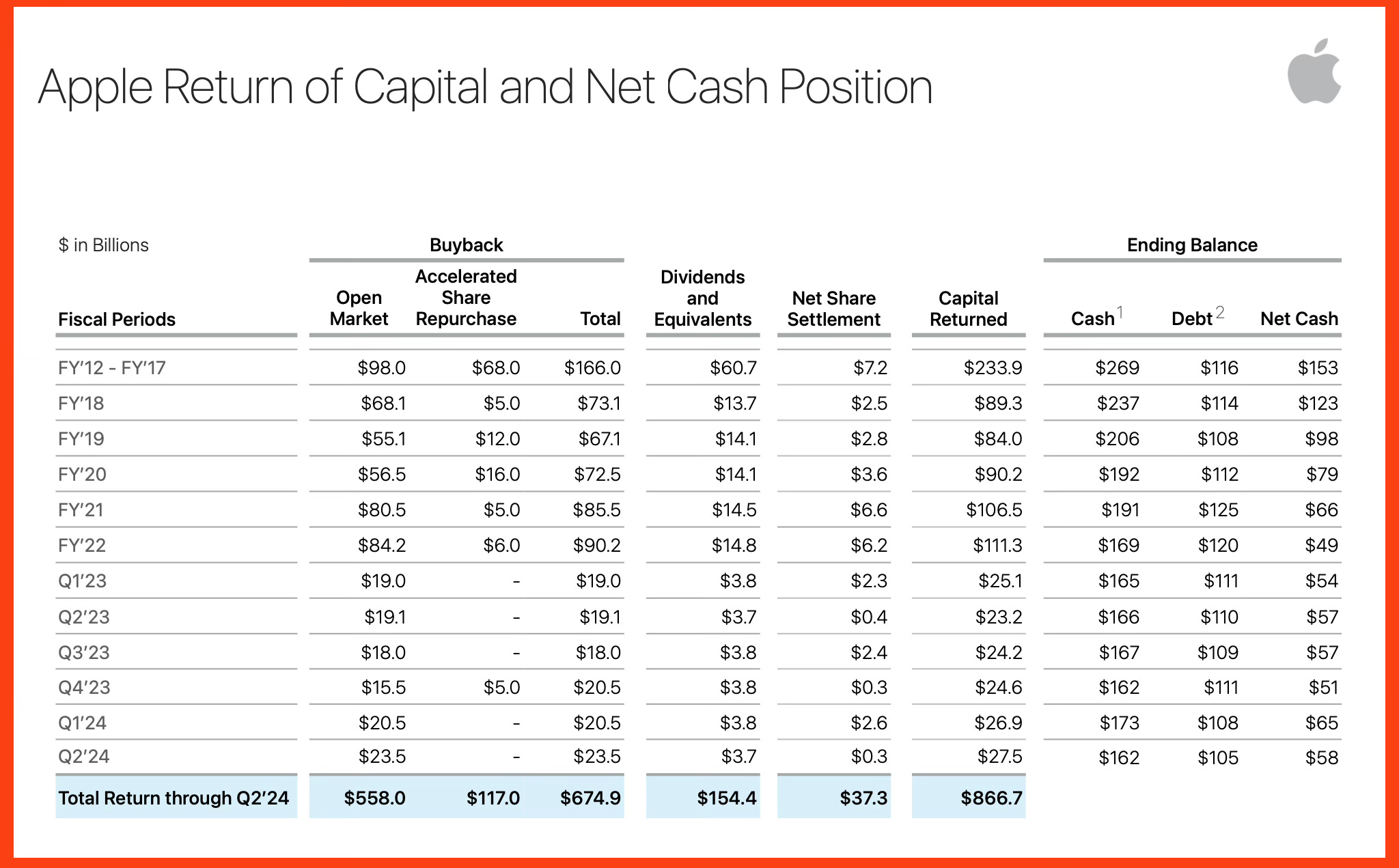

Capital Return History: AAPL

investor.apple.com: [Copied & Pasted] Investor Updates > Additional Reports > Apple Return of Capital and Net Cash position

[Excerpt] “During the quarter, our record business performance generated EPS growth of 11 percent and nearly $29 billion in operating cash flow, allowing us to return over $32 billion to shareholders,” said Luca Maestri, Apple’s CFO. “We are also very pleased that our installed base of active devices reached a new all-time high in all geographic segments, thanks to very high levels of customer satisfaction and loyalty.” Source: Apple, Inc.

$AAPL's buyback program is working hard today! The only big tech green

$AAPL up 3% Trading at 32-33x forward P/E, Apple's 5% y/y growth in Q2 hardly justifies such investor enthusiasm, especially on a deep red day for broad equity indices. Apple buyback at work?

☑️ #14 Jul 19, 2024

The common misconception is they do this FOR shareholders

@ayela: Share buybacks do NOT give back to investors.

Companies repurchase their shares in programs they call BUYBACKS. When a company reduces the number of shares, it reduces the divisor and thus (1) increases the earnings per share and (2) increases the price of the stock.

The common misconception is they do this FOR shareholders. This could not be further from the truth as the number one cause behind share buybacks is EXECUTIVE PAY (Thurm, S. & Ng, 2013).

Most executives are paid a bonus on their earnings per share (EPS) at the end of the year, so what do they do when they cannot increase earnings? They reduce the number of shares, boosting EPS.

The sole reason for buying back your stock is if it is priced too low. However, statistically, share buybacks happen at the worst possible moments, the peaks (Lazonick & W., 2012).

This worsens the state of the companies, as this same cash could have been deployed to increase productivity or distributed as dividends.

Fried & J. M. (2010) touch upon a key component in the equation, long-term damage.

This version of corporate greed can damage a society permanently, as it incentivizes unproductive behavior.

StreetSmarts: But while Apple is the King of large buybacks, it doesn’t come close to some of its much smaller peers on a percentile basis. For example, Marathon Petroleum bought back 24% of it shares in 2023, following 29% and 13% in 2022 and 2021 respectively.

investor.apple.com: [Copied & Pasted] Investor Updates > Additional Reports > Apple Return of Capital and Net Cash position

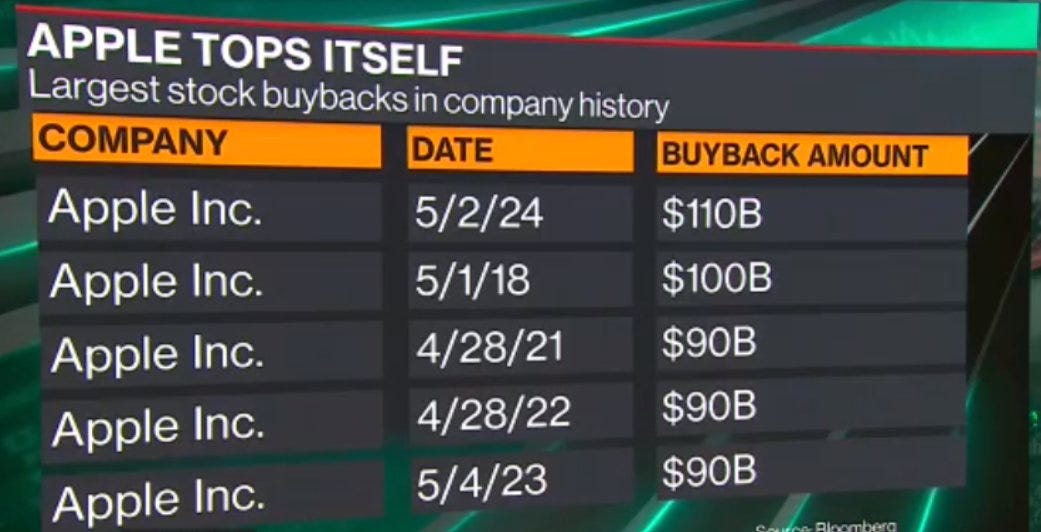

[Excerpt] Apple’s board of directors has declared a cash dividend of $0.25 per share of the Company’s common stock, an increase of 4 percent. The dividend is payable on May 16, 2024 to shareholders of record as of the close of business on May 13, 2024. The board of directors has also authorized an additional program to repurchase up to $110 billion of the Company’s common stock. Source: Apple, Inc.

1. Cash includes cash and cash equivalents, short-term and long-term marketable securities. 2. Debt includes commercial paper and repurchase agreements; as of June 29, 2024, the Company had $3.0 billion of commercial paper outstanding. Note: Numbers may not add precisely due to roundingSource: Apple, Inc.

🔹Related content:

@SpecialSitsNews: Largest individual company buybacks in company history... it's only $AAPL for the top 5 spots

- How does it make sense to increase buybacks during an investment phase into AI

- Getting to net cash neutral isn't a great goal

- Want cash to equal debt...

- $57bn of net cash now, going to 0

- Just CEO trying to boost his own incentive compensation..

@NasdaqExchange: On December 12, 1980, @Apple went public on @Nasdaq, raising more capital than any IPO since 1956. Apple not only transformed the computer industry, but also created relationships between tech and stock trading. Learn more as we celebrate #Nasdaq50:

SEC Adopts Amendments to Modernize Share Repurchase Disclosure

sec.gov: [Transcription] FOR IMMEDIATE RELEASE 2023-85. Washington D.C., May 3, 2023 — The Securities and Exchange Commission today adopted amendments to modernize the disclosure requirements relating to repurchases of an issuer’s equity securities, including requiring issuers to provide daily repurchase activity on a quarterly or semi-annual basis, depending on the type of issuer. The amendments will improve disclosure and provide investors with enhanced information to assess the purposes and effects of share repurchases.

“In 2021, buybacks amounted to nearly $950 billion and reportedly reached more than $1.25 trillion in 2022,”

“Today’s amendments will increase the transparency and integrity of this significant means by which issuers transact in their own securities. Through these disclosures, investors will be able to better assess issuer buyback programs. The disclosures will also help lessen some of the information asymmetries inherent between issuers and investors in buybacks. That’s good for investors, issuers, and the markets.”

SEC Chair Gary Gensler

The amendments will require issuers to disclose daily quantitative share repurchase information either quarterly or semi-annually. The required disclosures include, for each day on which a repurchase was conducted, the number of shares repurchased that day and the average price paid, among other things. Issuers will also be required to include a checkbox indicating whether certain officers and directors traded in the relevant securities in the four business days before or after the announcement of the repurchase plan or program.

Further, the amendments will revise and expand narrative repurchase disclosure requirements to require that an issuer disclose: (1) the objectives or rationales for its share repurchases and the process or criteria used to determine the amount of repurchases; and (2) any policies and procedures relating to purchases and sales of the issuer’s securities during a repurchase program by its officers and directors, including any restriction on such transactions.

Finally, the amendments will add a new item to Regulation S-K to better allow investors, the Commission, and other market participants to observe how issuers use Rule 10b5-1 plans. New Item 408(d) will require quarterly disclosure in periodic reports on Forms 10-Q and 10-K about an issuer’s adoption and termination of Rule 10b5-1 trading arrangements.

Foreign private issuers that file on foreign private issuer forms will disclose the quantitative data in new Form F-SR beginning with the Form F-SR that covers the first full fiscal quarter that begins on or after April 1, 2024, and provide the narrative disclosure starting in the first Form 20-F filed after their first Form F-SR has been filed. Registered closed-end management investment companies that are exchange traded will disclose the quantitative data and provide the narrative disclosure on Form N-CSR beginning with the Form N-CSR that covers the first six-month period that begins on or after January 1, 2024. All other issuers will be required to include the quantitative data as an exhibit to their Forms 10-Q and 10-K and provide the narrative disclosure in their Forms 10-Q and 10-K beginning with the first filing that covers the first full fiscal quarter that begins on or after October 1, 2023.

Buybacks from S&P 500 Companies Set Record in 2022

wsj.com: [Transcription] [Excerpts] Companies in the S&P 500 spent more money repurchasing their own shares in 2022 than any other calendar year in history, according to S&P Dow Jones Indices.

S&P 500 buybacks totaled $922.7 billion in 2022, up from $881.7 billion in 2021.

Buybacks in the fourth quarter of 2022 came in at $211.2 billion, up 0.2% from prior quarter and down about 22% from the fourth quarter of 2021.

Source: S&P Dow Jones Indices via The Wall Street Journal (last updated 3/21/23)

Warren Buffett’s Letters to Berkshire Shareholders: 2022

berkshirehathaway.com: An economic illiterate or a silver-tongued demagogue (characters that are not mutually exclusive)

[Transcription] [Excerpts] A very minor gain in per-share intrinsic value took place in 2022 through Berkshire share repurchases as well as similar moves at Apple and American Express, both significant investees of ours. At Berkshire, we directly increased your interest in our unique collection of businesses by repurchasing 1.2% of the company’s outstanding shares. At Apple and Amex, repurchases increased Berkshire’s ownership a bit without any cost to us.

The math isn’t complicated: When the share count goes down, your interest in our many businesses goes up. Every small bit helps if repurchases are made at value-accretive prices. Just as surely, when a company overpays for repurchases, the continuing shareholders lose. At such times, gains flow only to the selling shareholders and to the friendly, but expensive, investment banker who recommended the foolish purchases.

Gains from value-accretive repurchases, it should be emphasized, benefit all owners – in every respect. Imagine, if you will, three fully-informed shareholders of a local auto dealership, one of whom manages the business. Imagine, further, that one of the passive owners wishes to sell his interest back to the company at a price attractive to the two continuing shareholders. When completed, has this transaction harmed anyone? Is the manager somehow favored over the continuing passive owners? Has the public been hurt?

When you are told that all repurchases are harmful to shareholders or to the country, or particularly beneficial to CEOs, you are listening to either an economic illiterate or a silver-tongued demagogue (characters that are not mutually exclusive).

Almost endless details of Berkshire’s 2022 operations are laid out on pages K-33 – K-66. Charlie and I, along with many Berkshire shareholders, enjoy poring over the many facts and figures laid out in that section. These pages are not, however, required reading. There are many Berkshire centimillionaires and, yes, billionaires who have never studied our financial figures. They simply know that Charlie and I – along with our families and close friends – continue to have very significant investments in Berkshire, and they trust us to treat their money as we do our own.

SEC Reopens Comment Period for Proposed Rule on Share Repurchase Disclosure Modernization

sec.gov: [Transcription] FOR IMMEDIATE RELEASE 2022-216. Washington D.C., Dec. 7, 2022 — The Securities and Exchange Commission today reopened the comment period on proposed amendments intended to modernize and improve the disclosure required about an issuer’s repurchases of its equity securities, often referred to as buybacks.

The Commission is reopening the comment period because, after the proposed amendments were published for public comment, The Inflation Reduction Act of 2022 was enacted. The law imposes upon certain corporations a non-deductible excise tax equal to one percent of the fair market value of any stock of the corporation repurchased by such corporation during the taxable year. As a result, the Commission staff has prepared a memorandum that discusses potential economic effects of the new excise tax that may be helpful in evaluating the proposed amendments.

The amendments were initially proposed by the Commission in December 2021, and the comment period for the proposal was reopened in October 2022. The staff memorandum is available for review as part of the public comment file. The public comment period will remain open for 30 days after publication in the FederalRegister.

🔹Comments received: Comments on Share Repurchase Disclosure Modernization

🙂

🇺🇸 #4 Dec 15, 2021

SEC Proposes New Share Repurchase Disclosure Rules

sec.gov: [Transcription] The proposal would establish new Form SR for reporting issuer share repurchases and enhance existing periodic disclosure

FOR IMMEDIATE RELEASE 2021-257. Washington D.C., Dec. 15, 2021 — The Securities and Exchange Commission today proposed amendments to its rules regarding disclosure about an issuer’s repurchases of its equity securities, often referred to as buybacks.

"Share buybacks have become a significant component of how public issuers return capital to shareholders,"

"I think we can lessen the information asymmetries between issuers and investors through enhanced timeliness and granularity of disclosures that today’s proposal would provide."

SEC Chair Gary Gensler

The proposed rules would require an issuer to provide a new Form SR before the end of the first business day following the day the issuer executes a share repurchase. Form SR would require disclosure identifying the class of securities purchased, the total amount purchased, the average price paid, as well as the aggregate total amount purchased on the open market in reliance on the safe harbor in Exchange Act Rule 10b-18 or pursuant to a plan that is intended to satisfy the affirmative defense conditions of Exchange Act Rule 10b5-1(c).

The proposed amendments also would enhance existing periodic disclosure requirements regarding repurchases of an issuer’s equity securities. Specifically, the proposed amendments would require an issuer to disclose: the objective or rationale for the share repurchases and the process or criteria used to determine the repurchase amounts; any policies and procedures relating to purchases and sales of the issuer’s securities by its officers and directors during a repurchase program, including any restriction on such transactions; and whether the issuer is making its repurchases pursuant to a plan that it intends to satisfy the affirmative defense conditions of Exchange Act Rule 10b5-1(c) and/or the conditions of the Exchange Act Rule 10b-18 non-exclusive safe harbor.

The proposed rules apply to issuers that repurchase securities registered under Section 12 of the Securities Exchange Act of 1934, including foreign private issuers and certain registered closed-end funds.

The proposing release will be published on SEC.gov and in the Federal Register. The comment period will remain open for 45 days after publication in the Federal Register.

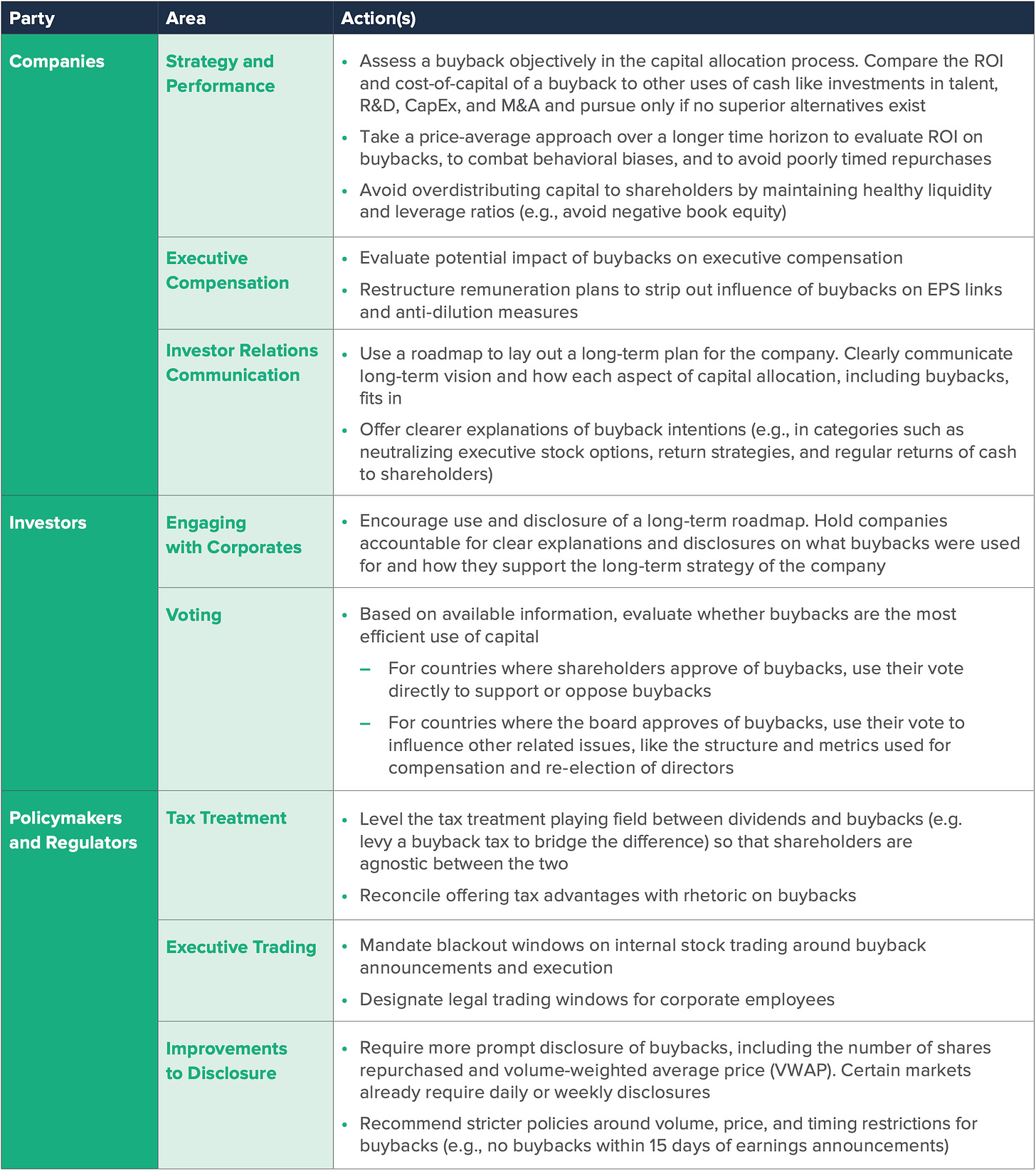

The Dangers of Buybacks: Mitigating Common Pitfalls

fcltglobal.org: Returning capital to shareholders is an important and legitimate goal of many corporations. Buybacks are often an effective way to distribute capital, but care must be taken to mitigate downfalls related to personal gain and enrichment, poor timing, and excess leverage.

Buybacks have experienced a meteoric rise in popularity since the turn of the twenty-first century, overtaking dividends as the preferred means to return capital to shareholders in jurisdictions like the US. In 2019 alone, corporations spent more than USD 1.2 trillion globally on buybacks.

But the rise of buybacks has been riddled with controversy. Academics, practitioners, and politicians alike have maligned the use of buybacks, taking issue with their potential contribution to income inequality, underinvestment in innovation, and use for personal enrichment. Buybacks and their implications for the long-term strength of the economy are controversial but not well understood.

Buybacks Playbook: In the right circumstances, buybacks can further long-term goals; new tools and guidelines could help evaluate buybacks on their long-term merits.

Source: FTCGlobal

🙂

🇺🇸 #2 Nov 10, 2003

Purchases of Certain Equity Securities by the Issuer and Others

sec.gov: [Transcriptions] [Excerpts] The proposal would establish new Form SR for reporting issuer share repurchases and enhance existing periodic disclosure

SUMMARY: We are adopting amendments to Rule 10b–18 under the Securities Exchange Act of 1934 (Exchange Act), which provides issuers with a ‘‘safe harbor’’ from liability for manipulation when they repurchase their common stock in the market in accordance with the Rule’s manner, timing, price, and volume conditions. The amendments are intended to simplify and update the safe harbor provisions in light of market developments since the Rule’s adoption. To enhance the transparency of issuer repurchases, we also are adopting amendments to a number of regulations and forms to require disclosure of all issuer repurchases (open market and private transactions), regardless of whether the repurchases are effected in accordance with the safe harbor rule.

§240.10b–18 Purchases of certain eq- uity securities by the issuer and others.

PRELIMINARY NOTES TO §240.10b–18 1. Section 240.10b–18 provides an issuer (and its affiliated purchasers) with a ‘‘safe harbor’’ from liability for manipulation under sections 9(a)(2) of the Act and §240.10b–5 under the Act solely by reason of the manner, timing, price, and volume of their repurchases when they repurchase the issuer’s common stock in the market in accordance with the section’s manner, timing, price, and volume conditions. As a safe harbor, compliance with § 240.10b–18 is voluntary. To come within the safe harbor, however, an issuer’s repurchases must satisfy (on a daily basis) each of the section’s four conditions. Failure to meet any one of the four conditions will remove all of the issuer’s repurchases from the safe harbor for that day. The safe harbor, moreover, is not available for repurchases that, although made in technical compliance with the section, are part of a plan or scheme to evade the federal securities laws.

2. Regardless of whether the repurchases are effected in accordance with §240.10b–18, reporting issuers must report their repurchasing activity as required by Item 703 of Regulations S-K and S-B (17 CFR 229.703 and 228.703) and Item 15(e) of Form 20–F (17 CFR 249.220f) (regarding foreign private issuers), and closed-end management investment companies that are registered under the In- vestment Company Act of 1940 must report their repurchasing activity as required by fItem 8 of Form N-CSR (17 CFR 249.331; 17 CFR 274.128).

(a) Definitions. Unless otherwise provided, all terms used in this section shall have the same meaning as in the Act. In addition, the following definitions shall apply:

(1) ADTV means the average daily trading volume reported for the security during the four calendar weeks preceding the week in which the Rule 10b–18 purchase is to be effected.

(2) Affiliate means any person that directly or indirectly controls, is con- trolled by, or is under common control with, the issuer.

(3) Affiliated purchaser means:

(i) A person acting, directly or indirectly, in concert with the issuer for the purpose of acquiring the issuer’s securities; or

(ii) An affiliate who, directly or indirectly, controls the issuer’s purchases of such securities, whose purchases are controlled by the issuer, or whose purchases are under common control with those of the issuer; Provided, however, that ‘‘affiliated purchaser’’ shall not include a broker, dealer, or other person solely by reason of such broker, dealer, or other person effecting Rule 10b–18 purchases on behalf of the issuer or for its account, and shall not include an officer or director of the issuer solely by reason of that officer or director’s participation in the decision to authorize Rule 10b–18 purchases by or on behalf of the issuer.

(4) Agent independent of the issuer has the meaning contained in §242.100 of this chapter.

(5) Block means a quantity of stock that either:

(i) Has a purchase price of $200,000 or more; or

(ii) Is at least 5,000 shares and has a purchase price of at least $50,000; or

(iii) Is at least 20 round lots of the security and totals 150 percent or more of the trading volume for that security or, in the event that trading volume data are unavailable, is at least 20 round lots of the security and totals at least one-tenth of one percent (.001) of the outstanding shares of the security, exclusive of any shares owned by any affiliate; Provided, however, That a block under paragraph (a)(5)(i), (ii), and (iii) shall not include any amount a broker or dealer, acting as principal, has accumulated for the purpose of sale or resale to the issuer or to any affiliated purchaser of the issuer if the issuer or such affiliated purchaser knows or has reason to know that such amount was accumulated for such purpose, nor shall it include any amount that a broker or dealer has sold short to the issuer or to any affiliated purchaser of the issuer if the issuer or such affiliated purchaser knows or has reason to know that the sale was a short sale.

(6) Consolidated system means a consolidated transaction or quotation re- porting system that collects and publicly disseminates on a current and continuous basis transaction or quotation information in common equity securities pursuant to an effective transaction reporting plan or an effective national market system plan (as those terms are defined in §242.600 of this chapter).

(7) Market-wide trading suspension means a market-wide trading halt of 30 minutes or more that is:

(i) Imposed pursuant to the rules of a national securities exchange or a national securities association in response to a market-wide decline during a single trading session; or

(ii) Declared by the Commission pursuant to its authority under section 12(k) of the Act (15 U.S.C. 78l (k)).

(8) Plan has the meaning contained in § 242.100 of this chapter.

(9) Principal market for a security means the single securities market with the largest reported trading volume for the security during the six full calendar months preceding the week in which the Rule 10b–18 purchase is to be effected.

(10) Public float value has the meaning contained in § 242.100 of this chapter.

(11) Purchase price means the price paid per share as reported, exclusive of any commission paid to a broker acting as agent, or commission equivalent, mark-up, or differential paid to a dealer.

(12) Riskless principal transaction means a transaction in which a broker or dealer after having received an order from an issuer to buy its security, buys the security as principal in the market at the same price to satisfy the issuer’s buy order. The issuer’s buy order must be effected at the same price per-share at which the broker or dealer bought the shares to satisfy the issuer’s buy order, exclusive of any explicitly disclosed markup or markdown, commission equivalent, or other fee. In addition, only the first leg of the transaction, when the broker or dealer buys the security in the market as principal, is reported under the rules of a self-regulatory organization or under the Act. For purposes of this section, the broker or dealer must have written policies and procedures in place to assure that, at a minimum, the issuer’s buy order was received prior to the offsetting transaction; the offsetting transaction is allocated to a riskless principal account or the issuer’s account within 60 seconds of the execution; and the broker or dealer has supervisory systems in place to produce records that enable the broker or dealer to accurately and readily reconstruct, in a time-sequenced manner, all orders effected on a riskless principal basis.

(13) Rule 10b–18 purchase means a pur- chase (or any bid or limit order that would effect such purchase) of an issuer’s common stock (or an equiva- lent interest, including a unit of bene- ficial interest in a trust or limited partnership or a depository share) by or for the issuer or any affiliated pur- chaser (including riskless principal transactions). However, it does not in- clude any purchase of such security:

(i) Effected during the applicable re- stricted period of a distribution that is subject to § 242.102 of this chapter;

(ii) Effected by or for an issuer plan by an agent independent of the issuer; (iii) Effected as a fractional share purchase (a fractional interest in a security) evidenced by a script certificate, order form, or similar document; (iv) Effected during the period from the time of public announcement (as defined in §230.165(f)) of a merger, acquisition, or similar transaction involving a recapitalization, until the earlier of the completion of such trans- action or the completion of the vote by target shareholders. This exclusion does not apply to Rule 10b–18 purchases:

(A) Effected during such transactionin which the consideration is solely cash and there is no valuation period; or

(B) Where:

(1) The total volume of Rule 10b–18 purchases effected on any single day does not exceed the lesser of 25% of the security’s four-week ADTV or the issuer’s average daily Rule 10b–18 pur- chases during the three full calendar months preceding the date of the an- nouncement of such transaction;

(2) The issuer’s block purchases effected pursuant to paragraph (b)(4) of this section do not exceed the average size and frequency of the issuer’s block purchases effected pursuant to paragraph (b)(4) of this section during the three full calendar months preceding the date of the announcement of such transaction; and

(3) Such purchases are not otherwise restricted or prohibited;

(v) Effected pursuant to § 240.13e-1;

(vi) Effected pursuant to a tender offer that is subject to § 240.13e-4 or specifically excepted from § 240.13e-4; or

(vii) Effected pursuant to a tender offer that is subject to section 14(d) of the Act (15 U.S.C. 78n(d)) and the rules and regulations thereunder.

(b) Conditions to be met. Rule 10b–18 purchases shall not be deemed to have violated the anti-manipulation provisions of sections 9(a)(2) or 10(b) of the Act (15 U.S.C. 78i(a)(2) or 78j(b)), or §240.10b–5 under the Act, solely by rea- son of the time, price, or amount of the Rule 10b–18 purchases, or the number of brokers or dealers used in connection with such purchases, if the issuer or affiliated purchaser of the issuer effects the Rule 10b–18 purchases according to each of the following conditions:

(1) One broker or dealer. Rule 10b–18 purchases must be effected from or through only one broker or dealer on any single day; Provided, however, that:

(i) The ‘‘one broker or dealer’’ condition shall not apply to Rule 10b–18 purchases that are not solicited by or on behalf of the issuer or its affiliated purchaser(s);

(ii) Where Rule 10b–18 purchases are effected by or on behalf of more than one affiliated purchaser of the issuer (or the issuer and one or more of its affiliated purchasers) on a single day, the issuer and all affiliated purchasers must use the same broker or dealer; and

(iii) Where Rule 10b–18 purchases are effected on behalf of the issuer by a broker-dealer that is not an electronic communication network (ECN) or other alternative trading system (ATS), that broker-dealer can access ECN or other ATS liquidity in order to execute repurchases on behalf of the issuer (or any affiliated purchaser of the issuer) on that day.

(2) Time of purchases. Rule 10b–18 purchases must not be:

(i) The opening (regular way) purchase reported in the consolidated system;

(ii) Effected during the 10 minutes before the scheduled close of the primary trading session in the principal market for the security, and the 10 minutes before the scheduled close of the primary trading session in the market where the purchase is effected, for a security that has an ADTV value of $1 million or more and a public float value of $150 million or more; and

(iii) Effected during the 30 minutes before the scheduled close of the primary trading session in the principal market for the security, and the 30 minutes before the scheduled close of the primary trading session in the market where the purchase is effected, for all other securities;

(iv) However, for purposes of this section, Rule 10b–18 purchases may be effected following the close of the primary trading session until the termination of the period in which last sale prices are reported in the consolidated system so long as such purchases are effected at prices that do not exceed the lower of the closing price of the primary trading session in the principal market for the security and any lower bids or sale prices subsequently reported in the consolidated system, and all of this section’s conditions are met. However, for purposes of this section, the issuer may use one broker or dealer to effect Rule 10b–18 purchases during this period that may be different from the broker or dealer that it used during the primary trading session. However, the issuer’s Rule 10b–18 purchase may not be the opening transaction of the session following the close of the primary trading session.

(3) Price of purchases. Rule 10b–18 purchases must be effected at a purchase price that:

(i) Does not exceed the highest independent bid or the last independent transaction price, whichever is higher, quoted or reported in the consolidated system at the time the Rule 10b–18 pur- chase is effected;

(ii) For securities for which bids and transaction prices are not quoted or re- ported in the consolidated system, Rule 10b–18 purchases must be effected at a purchase price that does not ex- ceed the highest independent bid or the last independent transaction price, whichever is higher, displayed and dis- seminated on any national securities exchange or on any inter-dealer quotation system (as defined in §240.15c2–11) that displays at least two priced quotations for the security, at the time the Rule 10b–18 purchase is ef- fected; and

(iii) For all other securities, Rule 10b–18 purchases must be effected at a price no higher than the highest inde- pendent bid obtained from three inde- pendent dealers.

(4) Volume of purchases. The total vol- ume of Rule 10b–18 purchases effected by or for the issuer and any affiliated purchasers effected on any single day must not exceed 25 percent of the ADTV for that security; However, once each week, in lieu of purchasing under the 25 percent of ADTV limit for that day, the issuer or an affiliated pur- chaser of the issuer may effect one block purchase if:

(i) No other Rule 10b–18 purchases are effected that day, and

(ii) The block purchase is not in- cluded when calculating a security’s four week ADTV under this section.

(c) Alternative conditions. The condi- tions of paragraph (b) of this section shall apply in connection with Rule 10b–18 purchases effected during a trad- ing session following the imposition of a market-wide trading suspension, ex- cept:

(1) That the time of purchases condi- tion in paragraph (b)(2) of this section shall not apply, either:

(i) From the reopening of trading until the scheduled close of trading on the day that the market-wide trading suspension is imposed; or

(ii) At the opening of trading on the next trading day until the scheduled close of trading that day, if a market- wide trading suspension was in effect at the close of trading on the preceding day; and

(2) The volume of purchases condi- tion in paragraph (b)(4) of this section is modified so that the amount of Rule 10b–18 purchases must not exceed 100 percent of the ADTV for that security.

(d) Other purchases. No presumption shall arise that an issuer or an affili- ated purchaser has violated the anti- manipulation provisions of sections 9(a)(2) or 10(b) of the Act (15 U.S.C. 78i(a)(2) or 78j(b)), or §240.10b–5 under the Act, if the Rule 10b–18 purchases of such issuer or affiliated purchaser do not meet the conditions specified in paragraph (b) or (c) of this section.

[68 FR 64970, Nov. 17, 2003, as amended at 70 FR 37618, June 29, 2005]

§240.10b–21 Deception in connection with a seller’s ability or intent to deliver securities on the date deliv- ery is due.

PRELIMINARY NOTE TO §240.10b–21: This rule is not intended to limit, or restrict, the ap- plicability of the general antifraud provi- sions of the federal securities laws, such as section 10(b) of the Act and rule 10b–5 there- under.

(a) It shall also constitute a ‘‘ma- nipulative or deceptive device or con- trivance’’ as used in section 10(b) of this Act for any person to submit an order to sell an equity security if such person deceives a broker or dealer, a participant of a registered clearing agency, or a purchaser about its inten- tion or ability to deliver the security on or before the settlement date, and such person fails to deliver the security on or before the settlement date.

(b) For purposes of this rule, the term settlement date shall mean the business day on which delivery of a se- curity and payment of money is to be made through the facilities of a reg- istered clearing agency in connection with the sale of a security.

Over each of the last three years, investment gains and losses from changes in the market prices of our investments in equity securities produced significant volatility in our earnings. Berkshire’s common stock repurchase program, as amended, permits Berkshire to repurchase its Class A and Class B shares at prices below Berkshire’s intrinsic value, as conservatively determined by Warren Buffett, Berkshire’s Chairman of the Board and Chief Executive Officer, and Charlie Munger, Vice Chairman of the Board.

The program does not specify a maximum number of shares to be repurchased and does not require any specified repurchase amount. The program is expected to continue indefinitely. We will not repurchase our stock if it reduces the total amount of Berkshire’s consolidated cash, cash equivalents and U.S. Treasury Bill holdings below $30 billion.

Financial strength and redundant liquidity will always be of paramount importance at Berkshire. Berkshire paid $7.9 billion during 2022 to repurchase shares of its Class A and Class B common stock. At December 31, 2022, our insurance and other businesses held cash, cash equivalents and U.S. Treasury Bills of $125.0 billion, which included $94.7 billion in U.S. Treasury Bills.

Investments in equity and fixed maturity securities (excluding our investments in Kraft Heinz and Occidental common stock) were $333.9 billion.

Net earnings attributable to Berkshire shareholders was $35.5 billion in the first quarter of 2023, which included after-tax gains on our investments of $27.4 billion. Investment gains and losses from changes in the market prices of our investments in equity securities will produce significant volatility in our earnings.

Berkshire’s common stock repurchase program, as amended, permits Berkshire to repurchase its Class A and Class B shares at prices below Berkshire’s intrinsic value, as conservatively determined by Warren Buffett, Berkshire’s Chairman of the Board and Chief Executive Officer, and Charlie Munger, Vice Chairman of the Board. The program does not specify a maximum number of shares to be repurchased and does not require any specified repurchase amount.

The program is expected to continue indefinitely. We will not repurchase our stock if it reduces the total amount of Berkshire’s consolidated cash, cash equivalents and U.S. Treasury Bills holdings below $30 billion.

Financial strength and redundant liquidity will always be of paramount importance at Berkshire. Berkshire paid $4.4 billion in the first quarter of 2023 to repurchase shares of its Class A and B common stock.

At March 31, 2023, our insurance and other businesses held cash, cash equivalents and U.S. Treasury Bills of $127.7 billion, which included $106.9 billion in U.S. Treasury Bills.

Financial Condition Our Consolidated Balance Sheet continues to reflect very significant liquidity and a very strong capital base. Consolidated shareholders’ equity attributable to Berkshire shareholders at September 30, 2022 was $455.4 billion, a decrease of $50.8 billion since December 31, 2021.

Net loss attributable to Berkshire shareholders was $41.0 billion in the first nine months of 2022, which included after-tax losses on our investments of $64.9 billion. Investment gains and losses from changes in the market prices of our investments in equity securities will produce significant volatility in our earnings.

Berkshire’s common stock repurchase program, as amended, permits Berkshire to repurchase its Class A and Class B shares at prices below Berkshire’s intrinsic value, as conservatively determined by Warren Buffett, Berkshire’s Chairman of the Board and Chief Executive Officer, and Charlie Munger, Vice Chairman of the Board. The program does not specify a maximum number of shares to be repurchased and does not require any specified repurchase amount.

The program is expected to continue indefinitely. We will not repurchase our stock if it reduces the total amount of Berkshire’s consolidated cash, cash equivalents and U.S. Treasury Bills holdings below $30 billion.

Financial strength and redundant liquidity will always be of paramount importance at Berkshire.

Our Consolidated shareholders’ equity at June 30, 2023 was $539.9 billion, an increase of $66.5 billion since December 31, 2022. Net earnings attributable to Berkshire shareholders was $71.4 billion in the first six months of 2023, which included after-tax gains on our investments of $53.3 billion.

Investment gains and losses from changes in the market prices of our investments in equity securities will produce significant volatility in our earnings. Berkshire’s common stock repurchase program, as amended, permits Berkshire to repurchase its Class A and Class B shares at prices below Berkshire’s intrinsic value, as conservatively determined by Warren Buffett, Berkshire’s Chairman of the Board and Chief Executive Officer, and Charlie Munger, Vice Chairman of the Board.

The program does not specify a maximum number of shares to be repurchased and does not require any specified repurchase amount. The program is expected to continue indefinitely. We will not repurchase our stock if it reduces the total amount of Berkshire’s consolidated cash, cash equivalents and U.S. Treasury Bills holdings below $30 billion.

Financial strength and redundant liquidity will always be of paramount importance at Berkshire. Berkshire paid $5.8 billion in the first six months of 2023 to repurchase shares of its Class A and B common stock.

Charlie and I like to see gains in both areas, but our primary focus is on building operating earnings. Over time, the businesses we currently own should increase their aggregate earnings, and we hope also to purchase some large operations that will give us a further boost.

We now have eight subsidiaries that would each be included in the Fortune 500 were they stand-alone companies. That leaves only 492 to go. My task is clear, and I’m on the prowl. Share Repurchases Last September, we announced that Berkshire would repurchase its shares at a price of up to 110% of book value.

We were in the market for only a few days – buying $67 million of stock – before the price advanced beyond our limit. Nonetheless, the general importance of share repurchases suggests I should focus for a bit on the subject.

Charlie and I favor repurchases when two conditions are met: first, a company has ample funds to take care of the operational and liquidity needs of its business; second, its stock is selling at a material discount to the company’s intrinsic business value, conservatively calculated. We have witnessed many bouts of repurchasing that failed our second test.

Sometimes, of course, infractions – even serious ones – are innocent; many CEOs never stop believing their stock is cheap. In other instances, a less benign conclusion seems warranted. It doesn’t suffice to say that repurchases are being made to offset the dilution from stock issuances or simply because a company has excess cash.

Continuing shareholders are hurt unless shares are purchased below intrinsic value. The first law of capital allocation – whether the money is slated for acquisitions or share repurchases – is that what is smart at one price is dumb at another. (One CEO who always stresses the price/value factor in repurchase decisions is Jamie Dimon at J.P. Morgan; I recommend that you read his annual letter.)

In the end, it was 100% rational and there are very few CEOs about whom I can make that statement. The stock-repurchase situation is fascinating to me. That's because the answer is so simple. You do it when you are buying dollar bills at clear cut and significant discount and only then.

As a general observation I would say that most companies that repurchased shares 30 years ago were doing it for the right reasons, and most companies doing it now are wrong when doing so. Time after time, I see managers who are attempting to be fashionable or subconsciously hoping to support their stock.

Loews is a great example of a company that's always repurchased shares for the right reasons. I could give examples of the reverse, but I follow the dictum praise by name, criticize by category. Best regards Warren What Warren thinks...

With Wall Street in chaos, Fortune naturally went to Omaha looking for wisdom. Warren Buffett talks about the economy, the credit crisis, Bear Stearns, and more. By Nicholas Varchaver, (Fortune Magazine) If Berkshire Hathaway's annual meeting, scheduled for May 3 this year, is known as the Woodstock of Capitalism, then perhaps this is the equivalent of Bob Dylan playing a private show in his own house: Some 15 times a year Berkshire CEO Warren Buffett invites a group of business students for an intensive day of learning.

The students tour one or two of the company's businesses and then proceed to Berkshire (BRKA, Fortune 500) headquarters in downtown Omaha, where Buffett opens the floor to two hours of questions and answers. Later everyone repairs to one of his favorite restaurants, where he treats them to lunch and root beer floats.

Finally, each student gets the chance to pose for a photo with Buffett.

So, Bernie has won. 1. Motivation determines the morality of share repurchases BECKY QUICK: Right, this question comes from Denny Poland, a shareholder from Pittsburgh. “A prominent senator (Sen. Elizabeth Warren, D-Massachusetts) recently categorized share buybacks as a form of market manipulation.

You’ve often said that repurchasing shares at prices below intrinsic value benefits continuing shareholders. “Could you and Charlie please elaborate on the higher order effect that these share repurchases have on society?” WARREN BUFFETT: Yeah, they’re a way of — they’re a way of, essentially, of distributing cash to the people that want the cash when other co-owners mostly want you to reinvest. And it’s a savings vehicle.

If the four of us sitting at this table decided we’d buy a few Dairy Queen franchises, we form a little company, and we all put in a million dollars or something like that, and we buy the Dairy Queen franchises, and they’re doing well. And three of the four of us want to keep buying more Dairy Queen franchises.

And we’re not done building and saving for the future. And we’re in the wealth creation business. And the fourth one says, “Listen, I’ve gotten rich enough. I’d rather take some money out.” And, well, there’s only two ways to do it.

We can pay dividends to all four of us, three of us — of whom don’t want it. And we can repurchase the shares at a fair price — if it’s just the four of us — we pick out a fair price and the fourth one gets bought out of his interest.

I find it almost impossible to believe some of the arguments that are made that it’s terrible to repurchase shares from a partner if they want to get out of something (laughs) and you’re able to do it at prices advantageous to the people who are staying. And it helps slightly the person that wants out.

And a majority of the Berkshire shareholders — a great majority — we had a vote on dividends one time — we’ve got savers.

From time to time, such possibilities are both numerous and blatantly attractive. Today, though, we find little that excites us. That’s largely because of a truism: Long-term interest rates that are low push the prices of all productive investments upward, whether these are stocks, apartments, farms, oil wells, whatever.

Other factors influence valuations as well, but interest rates will always be important. Our final path to value creation is to repurchase Berkshire shares. Through that simple act, we increase your share of the many controlled and non-controlled businesses Berkshire owns.

When the price/value equation is right, this path is the easiest and most certain way for us to increase your wealth. (Alongside the accretion of value to continuing shareholders, a couple of other parties gain: Repurchases are modestly beneficial to the seller of the repurchased shares and to society as well.) 8 Periodically, as alternative paths become unattractive, repurchases make good sense for Berkshire’s owners. During the past two years, we therefore repurchased 9% of the shares that were outstanding at yearend 2019 for a total cost of $51.7 billion.

That expenditure left our continuing shareholders owning about 10% more of all Berkshire businesses, whether these are wholly-owned (such as BNSF and GEICO) or partly-owned (such as Coca-Cola and Moody’s). I want to underscore that for Berkshire repurchases to make sense, our shares must offer appropriate value.

We don’t want to overpay for the shares of other companies, and it would be value-destroying if we were to overpay when we are buying Berkshire. As of February 23, 2022, since yearend we repurchased additional shares at a cost of $1.2 billion.

Our appetite remains large but will always remain price-dependent. It should be noted that Berkshire’s buyback opportunities are limited because of its high-class investor base.

Thanks for reading Securitiex on Substack! Subscribe for free to receive new posts and support my work.

SECURITIEX ON SUBSTACK is not investment advice. Any opinions and thoughts in SECURITIEX ON SUBSTACK represent the curator/author’s opinion only. Personal due diligence and adequate research should be done before taking any investment position.

The analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security.

cash as % of total assets")